Introduction: The Strategic Importance of Securitisation Applications

The SARFAESI Act, 2002 revolutionized debt recovery in India. Banks and financial institutions gained statutory powers to enforce security interests without approaching courts. This legislation transformed the recovery landscape significantly. For legal practitioners, understanding this Act is essential.

A Securitisation Application before DRT serves as the primary remedy for aggrieved borrowers. Section 17 of the SARFAESI Act provides this crucial statutory remedy. Borrowers, guarantors, and affected third parties can challenge enforcement measures through this application.

Why Procedural Compliance Matters for Banking Lawyers

The stakes in these matters are exceptionally high. According to the Ministry of Finance, DRTs across India have disposed of over 75,000 Securitisation Applications involving approximately Rs. 5.97 lakh crores as per official data. Therefore, even minor procedural errors can lead to dismissal.

Banking lawyers must master both substantive and procedural aspects. The consequences of non-compliance extend beyond individual cases. Moreover, a dismissed application leaves borrowers without statutory protection against enforcement measures.

Currently, 39 DRTs and 5 DRATs operate across India. These tribunals handle enormous caseloads with significant financial implications. For example, in 2023-24 alone, DRTs disposed of 16,146 SA cases involving Rs. 1,41,684.93 crores. Consequently, procedural efficiency directly impacts recovery timelines for all stakeholders.

Determining Limitation Period: The Critical Timeline

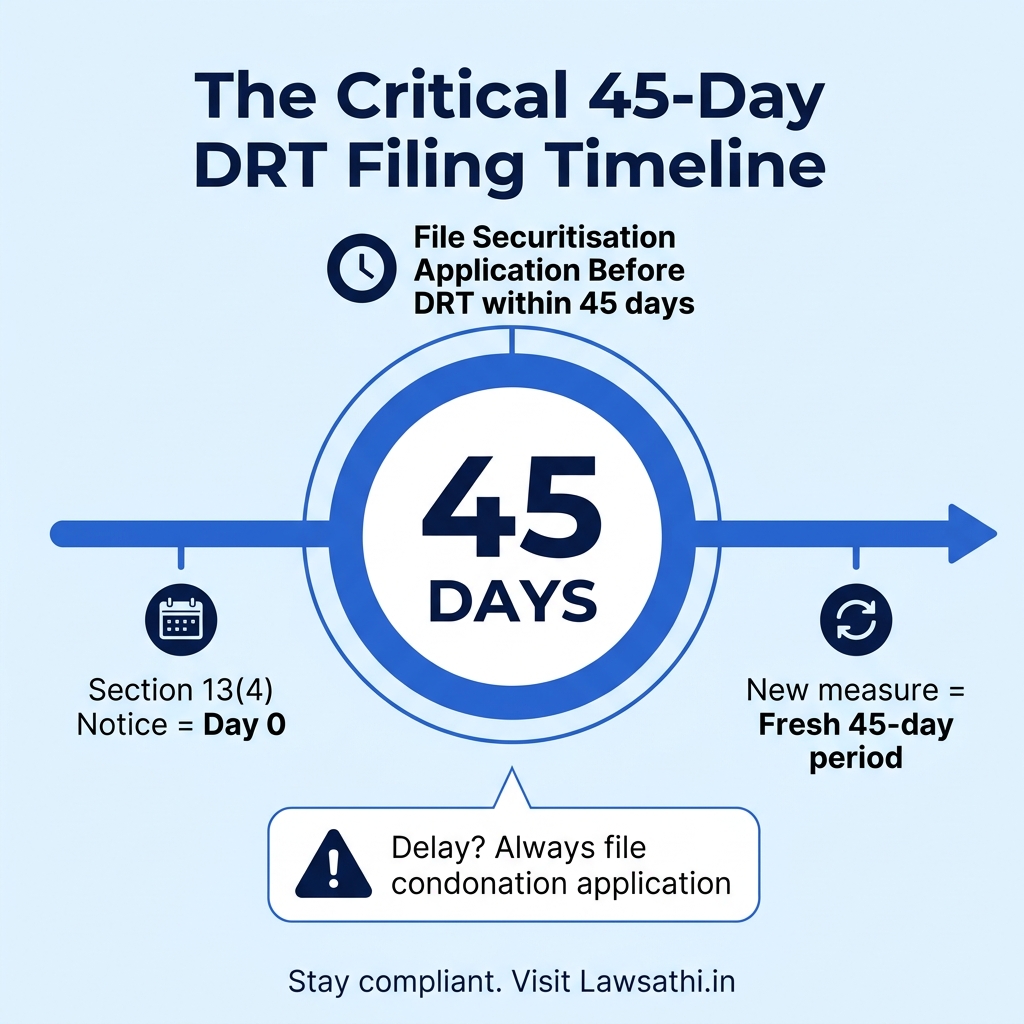

The limitation period stands as the most critical procedural aspect. A Securitisation Application before DRT must comply with strict timelines. Missing these deadlines can prove fatal to a borrower’s case.

The Standard 45-Day Limitation Under Section 17

Section 17(1) prescribes a 45-day limitation period. This period begins from the date a measure under Section 13(4) is taken by the secured creditor. Measures include taking possession, appointing a manager, or selling the secured asset.

The Supreme Court in Indian Overseas Bank v. Ashok Saw Mills (2009) established a crucial principle. The Court held that action under Section 13(4) constitutes a “continuing cause of action.” This interpretation significantly impacts limitation calculations.

The Continuing Cause of Action Doctrine

This doctrine fundamentally changes how lawyers must calculate limitation. Each new measure under Section 13(4) triggers a fresh 45-day period. For instance, a bank may take symbolic possession in January. However, if it issues a sale notice in March, limitation restarts from March.

The Telangana High Court in Alpine Pharmaceuticals v. Andhra Bank clarified this position. The Court held that limitation starts afresh with every new measure. Therefore, a borrower cannot be non-suited for not filing earlier when subsequent measures occur.

Condonation of Delay: Can DRT Extend the Timeline?

This question has divided courts across India. The proviso to Section 17 allows condonation of delay for “sufficient cause.” However, conflicting interpretations exist regarding the applicable period and authority.

View A – DRT Can Condone Delay Under Section 5, Limitation Act:

The Madhya Pradesh High Court in Aniruddh Singh v. ICICI Bank (2024) held that Section 5 of the Limitation Act applies. Specifically, the Court reasoned that SARFAESI Act does not expressly exclude Limitation Act provisions.

Similarly, the Madras High Court in Ponnusamy v. DRT supported this view. The Court emphasized that the right of redemption under Section 13(8) requires liberal interpretation. In other words, excluding condonation would defeat this statutory right.

View B – Strict Application of the 45-Day Limit:

Some courts have taken a contrary position. They view the SA as an original proceeding similar to a civil suit. Therefore, Section 5 of the Limitation Act should not apply.

The Supreme Court has yet to conclusively settle this debate. In Baleshwar Dayal Jaiswal v. Bank of India (2016), the Court recognized DRAT’s power to condone delay in appeals. However, whether this reasoning extends to Section 17 applications remains pending adjudication.

Practical Calculation Strategy for Lawyers

Given this legal uncertainty, prudence dictates filing within 45 days. If delay is unavoidable, always file a condonation application simultaneously. Additionally, document the “sufficient cause” thoroughly with supporting evidence.

For example, if possession notice was received on January 1, file by February 15. Do not wait until the last day to avoid technical complications. However, if a sale notice arrives later, calculate limitation from that date.

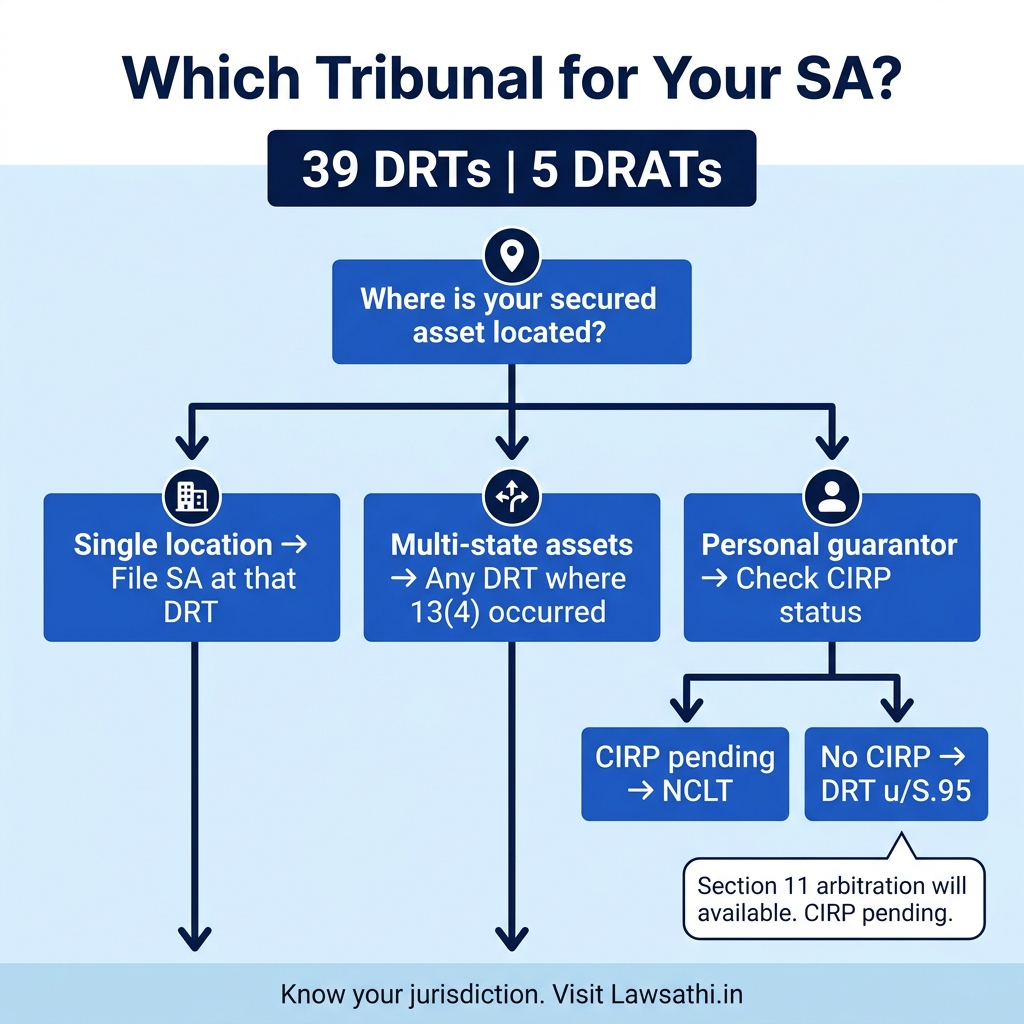

Jurisdictional Nuances: Which DRT to Approach?

Choosing the correct tribunal prevents procedural dismissals. Jurisdictional errors waste time and resources significantly. Therefore, understanding territorial jurisdiction rules is essential for every banking lawyer.

Territorial Jurisdiction Based on Asset Location

The general rule is straightforward. A Securitisation Application before DRT must be filed where the secured asset is located. Each DRT has defined territorial jurisdiction covering specific districts.

For instance, DRT-I Chennai covers Chennai South, Cuddalore, Kanchipuram, Karur, and several other districts. The DRT Chennai website provides detailed jurisdiction information.

When Secured Assets Span Multiple States

Complex situations arise when assets exist in multiple jurisdictions. The “cause of action” doctrine becomes relevant in such cases. If measures under Section 13(4) occur in multiple locations, borrowers have options.

They may approach any DRT where a measure has been taken. However, practical considerations favor choosing the principal asset location. This approach simplifies proceedings and evidence production.

Inter-Creditor Disputes: The Section 11 Bar

Recent Supreme Court jurisprudence has added a new dimension. In Bank of India v. Sri Nangli Rice Mills (2025 INSC 765), the Court addressed inter-creditor disputes.

Section 11 creates mandatory arbitration for disputes between banks, financial institutions, and ARCs. When both parties are financial entities, DRT lacks jurisdiction. Consequently, the proper forum is Section 11 arbitration.

Personal Guarantors: NCLT or DRT?

Another jurisdictional complexity involves personal guarantors. The relevant jurisprudence clarifies the position significantly.

If CIRP is pending against the corporate debtor, proceedings against personal guarantors lie before NCLT under Section 60 IBC. However, if no CIRP exists, the appropriate forum is DRT under Section 95 IBC.

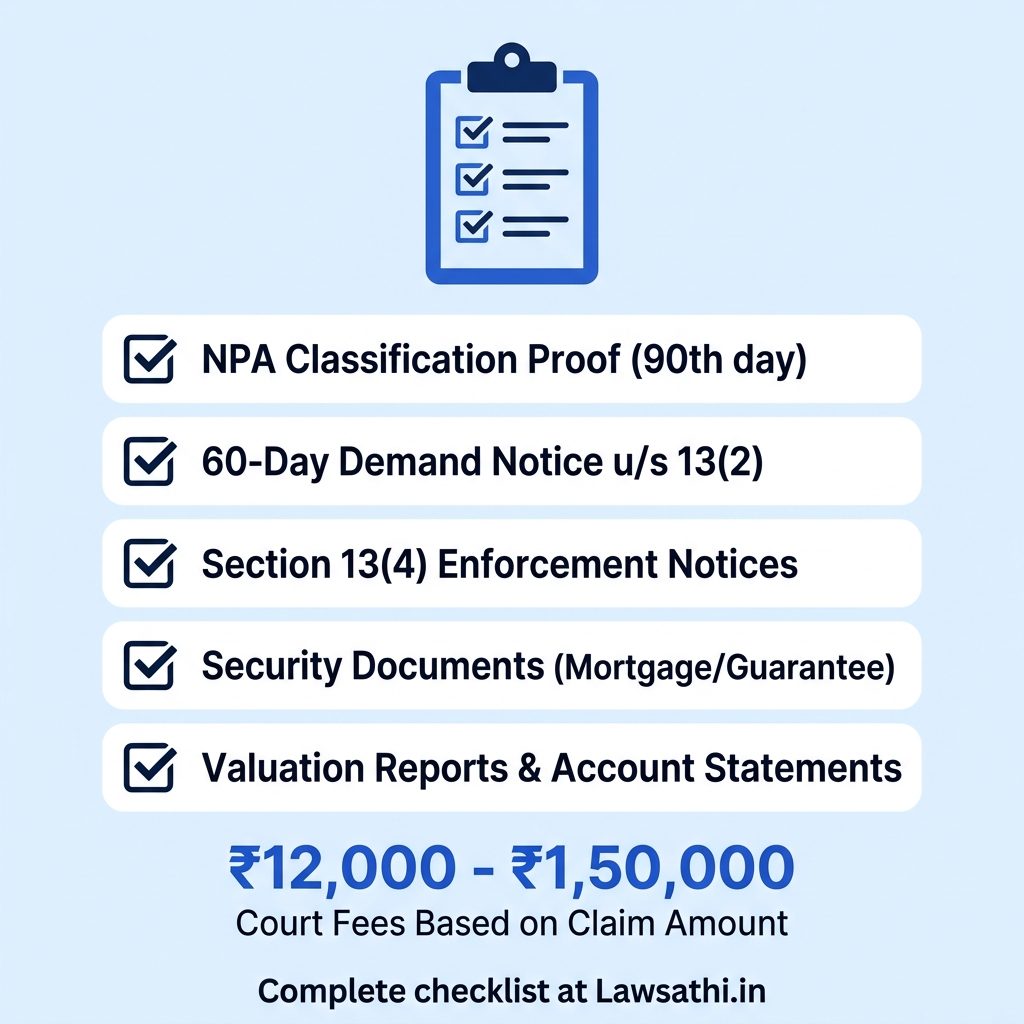

Mandatory Documentation Checklist for Filing

Complete documentation separates successful applications from dismissed ones. The DRT Registrar scrutinizes all filings strictly. Therefore, missing documents lead to defects and delays.

Proof of NPA Classification and Demand Notice

The application must evidence proper NPA classification. Include documents showing the account was declared NPA as per RBI guidelines. Moreover, the 60-day demand notice under Section 13(2) is fundamental.

According to recent Delhi High Court decisions-v.-karishma-enterprises-&-ors.,-2025-dhc-10911-db/view), classification on the 90th day is valid. The notice must demand full liability discharge within 60 days. Furthermore, proof of service is mandatory.

Evidence of Section 13(4) Measures

The application must attach all enforcement notices. This includes possession notices, sale notices, and auction publications. Additionally, each measure triggers separate cause of action rights.

Title Deeds and Security Interest Documents

Attach all security creation documents to establish the property interest. These include: – Mortgage deed or hypothecation agreement – Memorandum of deposit of title deeds – Security agreement – Guarantee deed

Discrepancies in property descriptions cause rejections frequently. Therefore, ensure survey numbers, boundaries, and area match exactly across documents.

Valuation Reports and Statement of Accounts

Include certified valuation reports as per SARFAESI Rules. The statement of accounts must be certified under the Bankers’ Books Evidence Act, 1891.

Additionally, the statement should show interest rate details. It must certify that penal interest has not been capitalized.

Affidavits, Verification, and Court Fees

Follow DRT Regulations 2015 for formatting requirements. Applications must be typed in English or Hindi. Furthermore, use Times New Roman font size 13 with double spacing.

Court fees vary based on claim amount. The DRAT fee structure provides guidance. For Original Applications, fees range from Rs. 12,000 to Rs. 1,50,000 maximum. However, Interlocutory Applications cost Rs. 250.

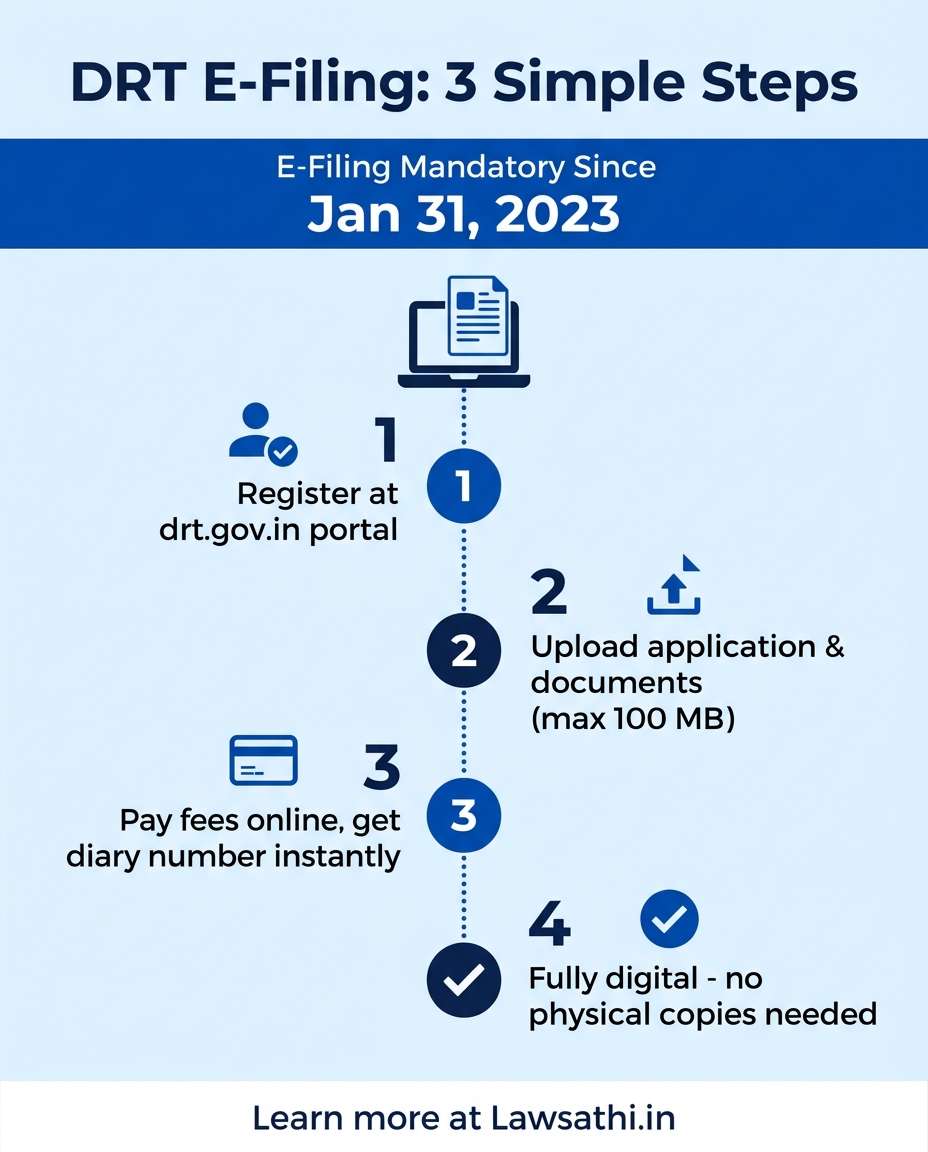

Step-by-Step Procedure: From Drafting to Registration

E-filing is now mandatory for all DRT filings since January 31, 2023. Understanding the e-filing portal is essential.

Pre-Filing Analysis: Assessing the Grievance

Before drafting, analyze the strength of the borrower’s case thoroughly. Review whether the bank followed all procedural requirements. Additionally, check NPA classification validity and notice compliance.

Identify which Section 13(4) measure triggered the cause of action. Calculate limitation accordingly with margin for safety.

Navigating the DRT E-Filing Portal

Step 1: User Registration

First, visit drt.gov.in and register as an External User. Create username and password credentials.

Step 2: Application Upload

The portal accepts four application types: OA, SA, MA, and IA. Upload the application with list of dates and supporting documents. Furthermore, maximum file size is 100 MB divided into four blocks of 25 MB each.

Step 3: Fee Payment and Diary Number

The system calculates fees automatically based on claim amount. Pay via net banking, debit card, credit card, or UPI. Upon successful payment, a diary number is generated instantly.

Scrutiny Process and Defect Curing

The Registrar scrutinizes all filed applications. Defects are communicated through the portal system. Therefore, applicants must cure defects within the stipulated time period.

The modification facility remains available during the defect-curing stage. Once all defects are resolved, the registration number is assigned.

Important Note on Hard Copies

After registration, hard copies need not be deposited physically. The entire process is digital. However, maintain physical records for your own reference and court proceedings.

Common Pitfalls Leading to Rejection

Understanding common errors helps avoid dismissals. Many applications fail on technical rather than substantive grounds.

Filing by Non-Eligible Applicants

Section 17 allows “any person aggrieved” to file applications. However, this includes borrowers, guarantors, and third parties with genuine interest. In contrast, mere tenants without legal property rights may lack standing.

The Supreme Court in Vishal N. Kalsaria v. Bank of India (2016) clarified statutory tenants’ position. Such tenants cannot be evicted under SARFAESI provisions. However, they can approach DRT under Section 17 for protection.

Discrepancies in Property Description

Inaccurate property descriptions frequently cause rejections. Survey numbers, boundaries, and area must match across all documents. Therefore, even minor discrepancies trigger defects.

Missing Statutory Notices

Failure to attach the Section 13(2) demand notice is fatal. Similarly, omission of Section 13(4) possession or sale notices leads to rejection. Always verify complete notice attachment before filing.

Defective Power of Attorney

Companies must file proper board resolutions authorizing representatives. Similarly, individual borrowers need properly executed power of attorney documents. However, expired authorizations invalidate the entire filing.

Post-Filing Strategy: Interim Relief and Hearings

Filing the Securitisation Application before DRT is only the first step. Strategic post-filing actions determine case outcomes significantly.

Seeking Stay Orders Against Property Sale

Interim relief is crucial in most SA cases. Borrowers typically seek stay against sale or transfer of property. The tribunal considers three factors: – Prima facie case strength – Balance of convenience – Irreparable injury possibility

For example, in SA No. 191/2024, DRT-I Delhi, third-party tenants challenged bank possession. Consequently, the DRT granted status quo pending adjudication.

Pre-Deposit Requirements for Appeals

For appeals to DRAT under Section 18, pre-deposit is mandatory. The Supreme Court in June 2024 upheld the 50% pre-deposit requirement.

The Kerala High Court in Kerala Gramin Bank v. Prajith Builders (2026) clarified an important aspect. Pre-deposit must be paid to DRAT directly. In other words, amount deposited with the lending bank cannot count as statutory pre-deposit.

However, not every DRT order requires pre-deposit for appeal. The Supreme Court indicated that appeals against procedural orders may be exempt.

Defense Strategy for Bank Representatives

Banking lawyers representing creditors should focus on compliance evidence. Recent judgments emphasize procedural adherence.

Key defenses include valid NPA classification and proper notice service. Compliance with Section 13(3A) regarding borrower objections strengthens the bank’s position. Additionally, proper sale procedure under Rules 8 and 9 is essential.

The Supreme Court in M. Rajendran v. KPK Oils (September 2025) highlighted interpretative issues. The Court urged the Ministry of Finance to address ambiguities in Section 13(8) and related rules.

Conclusion: Ensuring Procedural Compliance

Filing a Securitisation Application before DRT requires meticulous attention to detail. The 45-day limitation period demands immediate action upon receiving enforcement notices. Furthermore, understanding the continuing cause of action doctrine helps in limitation calculations.

Complete documentation is non-negotiable for successful filings. Missing notices or defective property descriptions lead to dismissals. Additionally, e-filing compliance through the DRT portal is now mandatory.

The jurisdictional analysis must be thorough before filing. Consider asset location, party status, and applicable provisions carefully. For inter-creditor disputes, Section 11 arbitration may apply instead.

Critical Timeline Summary

1. NPA classification after 90 days of default 2. Section 13(2) notice with 60-day compliance period 3. Section 13(4) measures after notice expiry 4. SA filing within 45 days of the measure 5. Condonation application if delay is unavoidable

Post-filing strategy determines ultimate success. Therefore, seek interim relief promptly when property disposal is imminent. Moreover, understand pre-deposit requirements before filing appeals to DRAT.

The evolving jurisprudence on condonation of delay requires careful monitoring. File within the prescribed period whenever possible to avoid uncertainty.

Streamline your Banking Litigation Practice. Manage DRT deadlines, auto-generate documentation checklists, and track limitation periods effortlessly with LawSathi. Start your free trial today.