Introduction: A Strategic Shift in Property Transaction Compliance

In a significant move, the Government of India has officially doubled the mandatory PAN threshold for property transactions. The limit has increased from ₹10 Lakh to ₹20 Lakh. This significant amendment came through the Income Tax Amendment Rules 2026, notified in early March 2026. For legal practitioners advising on conveyancing matters, this change represents a meaningful shift in compliance requirements. Specifically, the amendment directly impacts how lawyers structure property deals and advise clients on documentation requirements.

Contextualizing the Amendment

This modification forms part of the broader “Reform Express” initiative announced by the Prime Minister. According to the Budget Speech 2026-27, the Government has rolled out over 350 reforms since August 2025. These reforms target GST simplification, compliance rationalization, and reducing regulatory burdens across sectors. Therefore, the new PAN threshold property transaction limit aligns with the Government’s vision of “Viksit Bharat” (Developed India) by 2047.

Legal Significance for Practitioners

For advocates handling real estate matters, this amendment reduces documentation requirements for moderate-value transactions. However, it also introduces new considerations for due diligence. Lawyers must now carefully assess whether transactions fall below the enhanced threshold. Additionally, they must distinguish between PAN quoting requirements and TDS obligations. This article provides a comprehensive analysis of the legal implications and practical compliance strategies.

Decoding the Amendment: Section 139A and Rule 114B Modifications

Understanding the Legislative Framework

The amendment modifies the fifth proviso to Section 139A of the Income Tax Act, 1961. This section governs mandatory PAN quoting requirements for specified transactions. Additionally, corresponding changes appear in Rule 114B of the Income Tax Rules, 1962. The Finance Bill 2026 Explanatory Memorandum provides the detailed rationale behind these modifications.

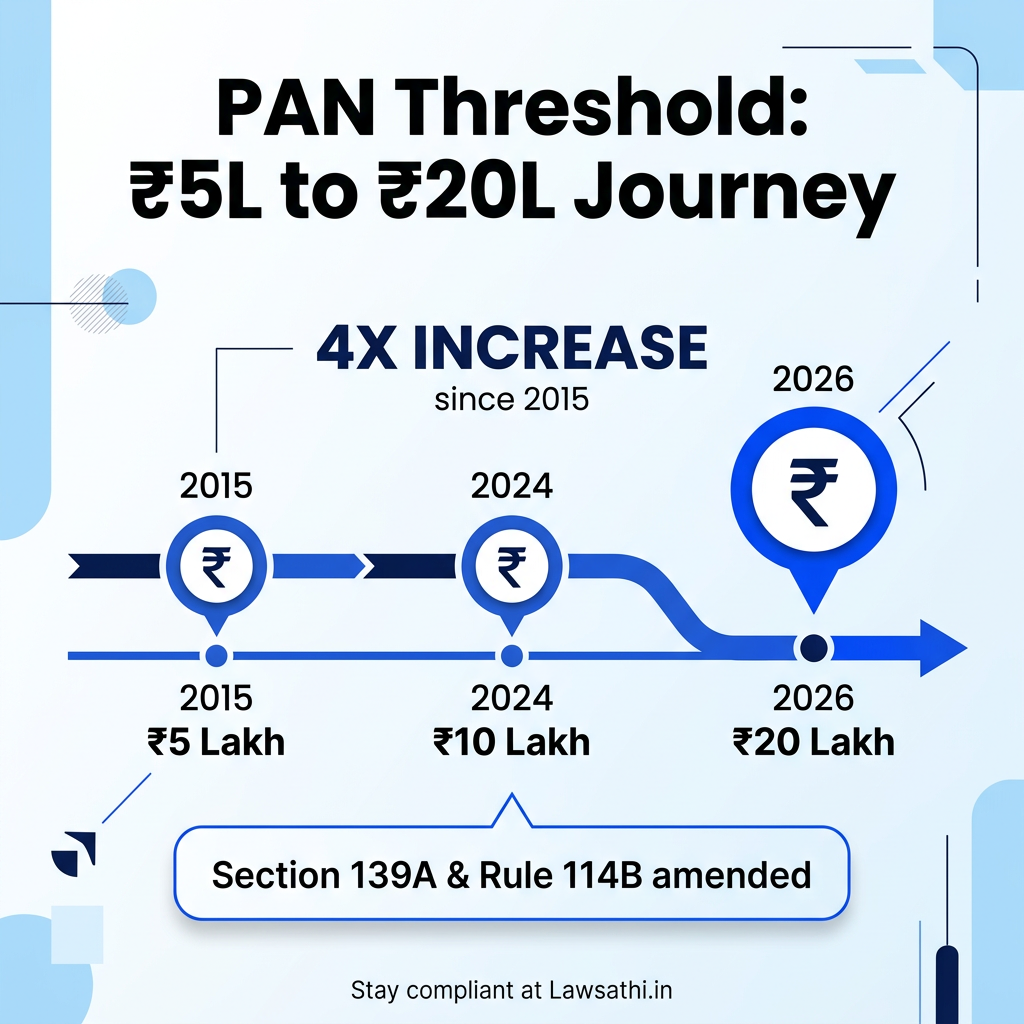

Previous vs. Current Threshold Structure

The evolution of PAN requirements for immovable property transactions shows a clear pattern:

As the table demonstrates, this represents the third increase in the PAN threshold property transaction limit since 2015. Each increase aims to reduce compliance burden on smaller transactions.

Scope of “Immovable Property” Under the New Rule

The term “immovable property” under Rule 114B covers land, buildings, and rights in such properties. However, agricultural land in rural areas generally falls outside this definition for Income Tax purposes. Therefore, transactions involving rural agricultural land may not trigger PAN requirements even if they exceed ₹20 Lakh. Lawyers must verify the classification of land before advising clients.

Furthermore, the threshold applies to both sale and purchase transactions. Both parties to a qualifying transaction must quote their PAN. If either party lacks a PAN, they must submit Form 60 as a declaration.

Stamp Valuation Authority’s Role

Importantly, the PAN threshold property transaction requirement considers stamp valuation. If the Stamp Valuation Authority values a property above ₹20 Lakh, PAN quoting becomes mandatory. This applies regardless of the actual transaction value stated in the sale agreement. Consequently, lawyers cannot advise clients to underquote consideration to avoid PAN requirements.

Critical Distinction: PAN Mandate vs. TDS Liability (Section 194-IA)

Clarifying the Common Confusion

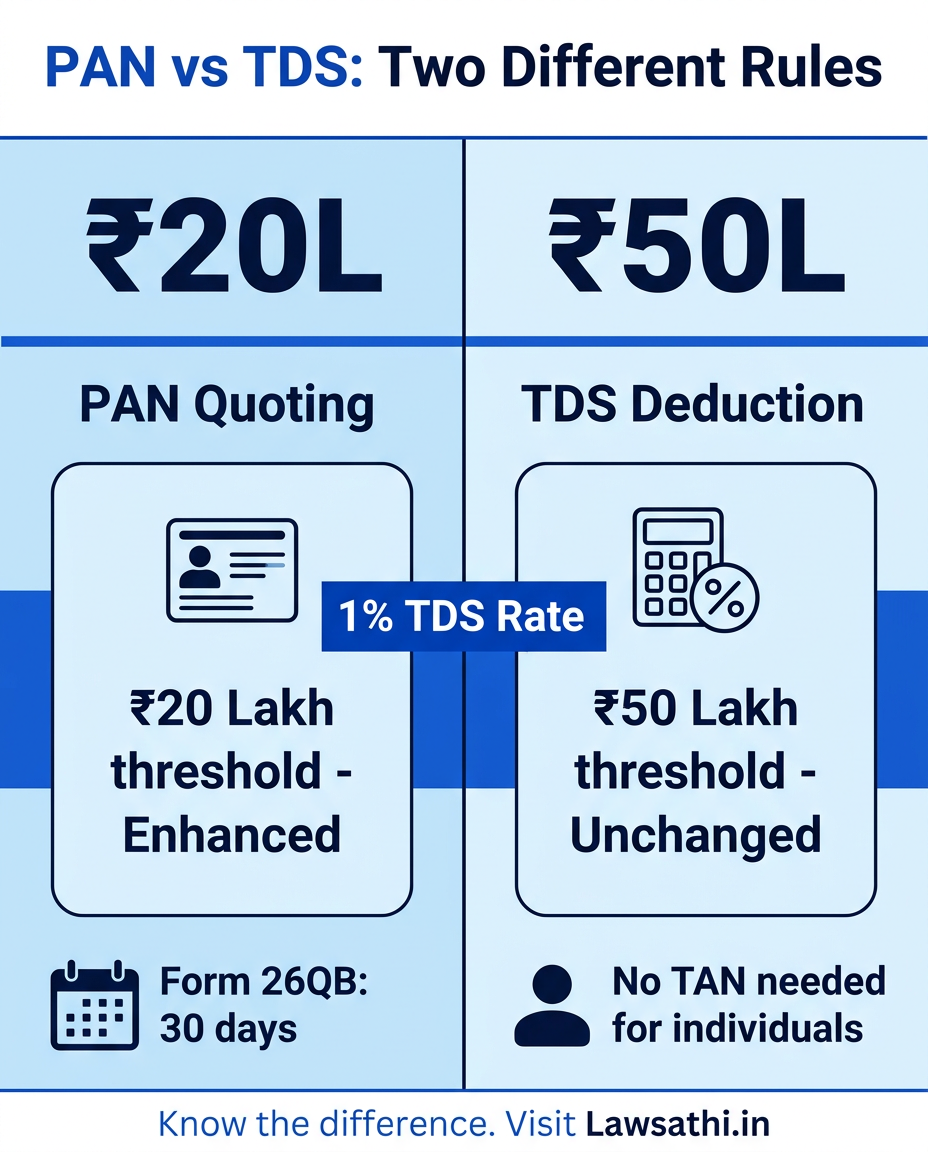

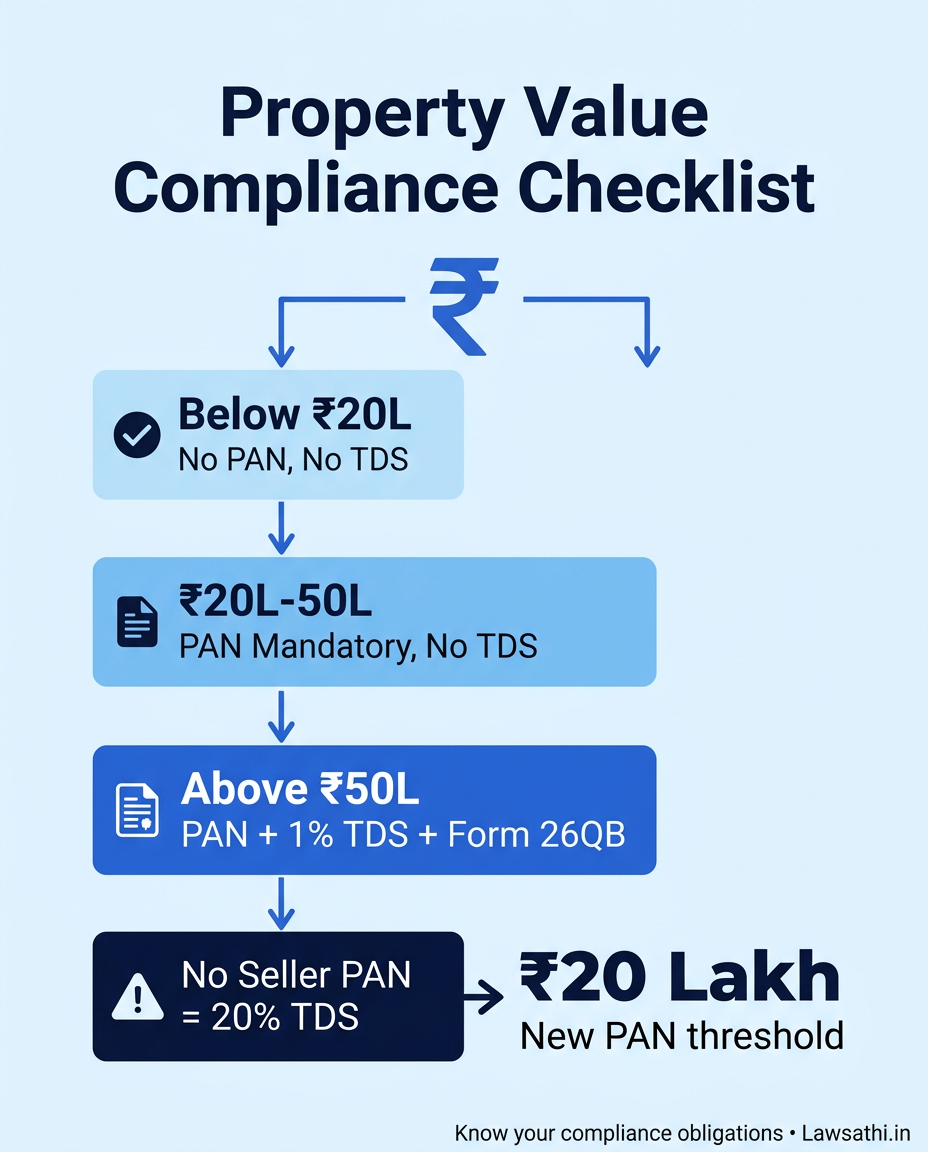

Many clients confuse PAN quoting requirements with TDS deduction obligations. In reality, these are entirely separate compliance frameworks under the Income Tax Act. The new PAN threshold property transaction limit of ₹20 Lakh does not affect TDS provisions. Therefore, lawyers must clearly explain this distinction to avoid compliance failures.

TDS Threshold Remains at ₹50 Lakh

Section 194-IA mandates TDS deduction at 1% on property transactions exceeding ₹50 Lakh. This threshold remains unchanged despite the PAN amendment. The Finance Bill 2026 confirms this position in Clause 75. For transactions above ₹50 Lakh, buyers must deduct TDS regardless of PAN requirements.

Practical Scenario Analysis

Consider a client purchasing property for ₹35 Lakh in a Tier-2 city. Under the new framework:

– PAN Quoting: Not required (below ₹20 Lakh threshold) – TDS Deduction: Not required (below ₹50 Lakh threshold) – Compliance: Only registration and stamp duty formalities apply

However, for a property valued at ₹55 Lakh:

– PAN Quoting: Required (exceeds ₹20 Lakh threshold) – TDS Deduction: Required at 1% (exceeds ₹50 Lakh threshold) – Form 26QB: Must be filed within 30 days of month-end

Form 26QB Filing Obligations

For transactions exceeding ₹50 Lakh, buyers must file Form 26QB with the Income Tax Department. This form captures TDS details and seller’s PAN. Even if the seller refuses to provide PAN, the buyer cannot escape liability. In such cases, TDS applies at the higher rate of 20% under Section 206AA.

New TAN Exemption for Individual Buyers

The Finance Bill 2026 introduces significant relief for individual property buyers. Resident individuals and HUFs purchasing property from non-residents previously required TAN (Tax Deduction Account Number). However, effective October 1, 2026, such buyers need not obtain TAN for property transactions. As a result, this reduces compliance burden significantly for one-time property purchasers.

Impact Analysis: Expanding the Formal Economy in Tier-2 & Tier-3 Cities

Benefits for Non-Metro Regions

The enhanced PAN threshold property transaction limit particularly benefits Tier-2 and Tier-3 cities. In these regions, property values typically range between ₹10-25 Lakh for residential units. The previous ₹10 Lakh threshold created compliance friction for most transactions. Now, transactions up to ₹20 Lakh proceed without PAN documentation requirements.

Relief for First-Time Homebuyers

First-time homebuyers form a significant portion of property purchasers in smaller cities. Many such buyers may not possess PAN cards or may have limited tax exposure. Previously, they had to either obtain PAN or submit Form 60 declarations. The new threshold eliminates this requirement for properties below ₹20 Lakh. Consequently, homebuyers face reduced paperwork and faster transaction processing.

Reduced Form 60 Submissions

Form 60 serves as a declaration for individuals without PAN entering specified transactions. The enhanced threshold significantly reduces Form 60 submissions for property deals. According to historical data from PIB releases, such reforms aim to reduce compliance burden on legitimate transactions. However, the Government continues capturing information on high-value deals through other mechanisms.

Risk of Structured Undervaluation

Legal practitioners must remain vigilant about potential undervaluation practices. Some parties may structure agreements to quote values just below ₹20 Lakh. However, the Stamp Valuation Authority’s valuation serves as a safeguard. If stamp value exceeds ₹20 Lakh, PAN requirements apply regardless of agreement value. Therefore, lawyers should advise clients against such manipulation attempts.

Professional Ethics Considerations

Advocates must not facilitate or encourage undervaluation to bypass compliance requirements. The Bar Council of India’s rules prohibit assisting in illegal or fraudulent activities. Therefore, lawyers should maintain accurate documentation of actual transaction values. This protects both the practitioner and the client from future litigation.

Compliance Checklist for Legal Practitioners

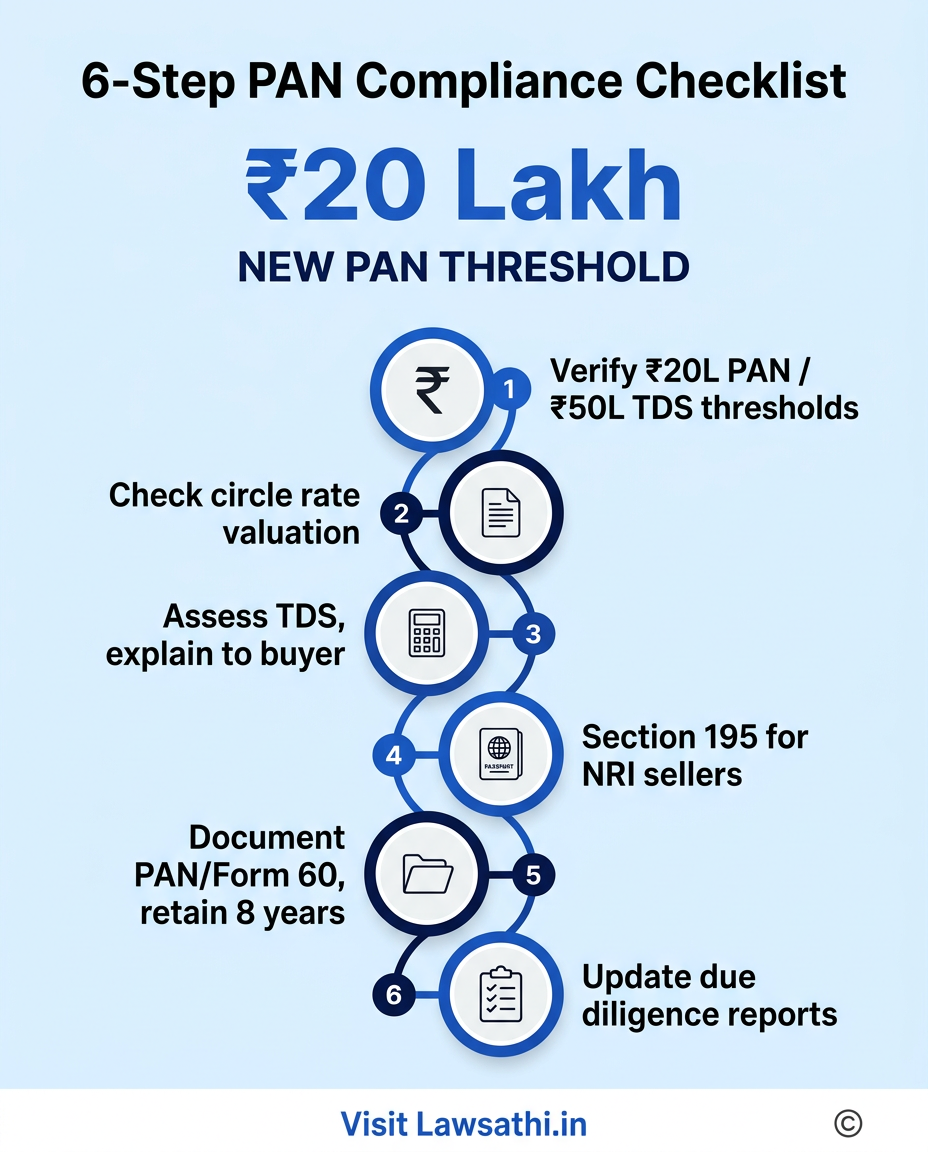

Step 1: Verify Transaction Value Against Thresholds

Before drafting sale agreements, lawyers must assess the transaction value. Specifically, compare the consideration amount with both ₹20 Lakh (PAN threshold) and ₹50 Lakh (TDS threshold). This determines applicable compliance requirements.

Step 2: Check Stamp Valuation Authority’s Rate

Obtain the circle rate or guidance value from local authorities. If stamp value exceeds ₹20 Lakh, advise clients to provide PAN copies. The higher of agreement value or stamp value governs PAN requirements. Therefore, always verify both figures before proceeding.

Step 3: Assess TDS Applicability

For transactions exceeding ₹50 Lakh, explain TDS obligations to buyer clients. The buyer must deduct 1% TDS and deposit it with the Income Tax Department. Furthermore, file Form 26QB within the prescribed timeline to avoid interest and penalties.

Step 4: Handle Non-Resident Sellers Carefully

Transactions involving non-resident sellers require additional due diligence. Section 195 provisions apply instead of Section 194-IA for non-resident sellers. However, the new TAN exemption helps individual buyers from October 2026. Therefore, verify seller’s residential status through passport and tax records.

Step 5: Document PAN or Form 60 Properly

For qualifying transactions, obtain PAN copies from both parties. If a party lacks PAN, collect Form 60 with complete details. Additionally, maintain these documents in your case file for at least 8 years. This satisfies professional obligations and assists in any future disputes.

Step 6: Update Due Diligence Reports

Title search reports should reflect the current PAN threshold property transaction compliance status. Include specific findings on applicable requirements based on transaction value. As a result, clients receive clear guidance on their obligations.

Conclusion: Balancing Ease of Business with Tax Enforcement

The doubling of the PAN threshold to ₹20 Lakh represents meaningful relief for property buyers in India. Millions of homebuyers in Tier-2 and Tier-3 cities benefit from reduced documentation requirements. The amendment aligns with the Government’s broader agenda of simplifying compliance. However, the distinction between PAN quoting and TDS deduction remains crucial for practitioners.

Future Outlook

The Budget 2026-27 speech emphasizes digital integration of land records with tax systems. Technologies like AI will serve as “force multipliers for better governance.” Therefore, lawyers should expect continued evolution in property transaction compliance frameworks.

The Lawyer’s Continuing Role

Despite relaxed PAN requirements, lawyers must ensure transparent and compliant transactions. Specifically, advise clients accurately on the interplay between agreement value and stamp value. Maintain proper due diligence and documentation practices. Above all, this protects client interests and upholds professional standards.

Simplify your firm’s real estate compliance tracking. Automate client document verification and TDS deadline alerts with LawSathi. Start your free trial today.