Budget 2026 has delivered a historic relief to farmers and landowners across India. The Finance Minister announced a complete exemption from income tax on compensation received from compulsory land acquisition. This Budget 2026 land acquisition tax exemption fundamentally changes the legal landscape for rural property disputes. Consequently, lawyers advising clients on land matters must immediately revise their strategies. Furthermore, the exemption applies to all awards and agreements made under the RFCTLARR Act, effective April 1, 2026.

Introduction: Budget 2026’s Landmark Tax Relief Announcement

The Union Budget 2026-27 introduced a significant welfare measure for the agricultural sector. Presented on February 1, 2026, it addresses long-standing concerns of farming communities. Finance Minister Nirmala Sitharaman announced that compensation from compulsory land acquisition will now be fully tax-exempt. This move aims to benefit an estimated 2.5 crore farmers. Previously, these farmers often faced protracted litigation over tax liabilities on their compensation amounts.

A Historic Shift in Taxation Policy

Previously, landowners faced complex tax calculations regarding the taxability of solatium and interest. Many endured lengthy litigation to resolve these disputes. However, the new amendment simplifies this completely. The Budget 2026 land acquisition tax exemption removes the tax burden entirely for individuals and Hindu Undivided Families (HUFs). According to the Budget Speech 2026-27 PDF, this provision applies from Assessment Year 2026-27. For legal practitioners, this represents a major shift in advisory work.

Why This Matters for Legal Practitioners

This amendment impacts thousands of pending cases across various courts and tribunals. Lawyers must now identify clients who can claim refunds for past taxes paid. Additionally, ongoing litigation regarding the taxability of interest and solatium requires immediate reconsideration. The public capital expenditure has increased from ₹2 lakh crore in 2014 to ₹12.2 lakh crore in 2026. Therefore, land acquisition for infrastructure projects will continue to rise. As a result, this exemption becomes highly relevant for future cases.

Understanding Section 96: The Legal Framework Explained

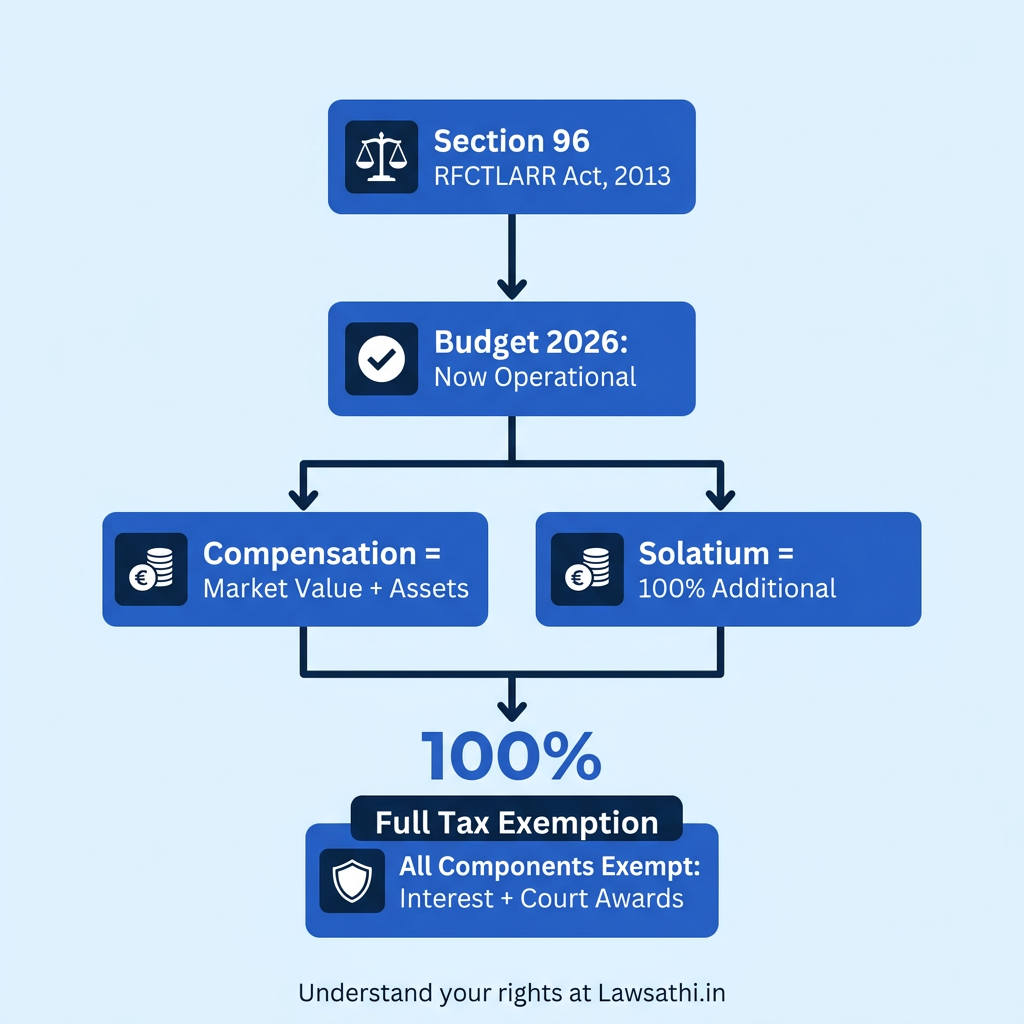

To fully grasp this exemption, lawyers must understand the source of this tax relief. Section 96 of the RFCTLARR Act, 2013, explicitly mandates a critical provision. Specifically, it states that no income tax shall be levied on any award or agreement made under this Act. Budget 2026 effectively operationalizes this provision within the Income Tax framework.

Clarifying the Legislative Framework

The RFCTLARR Act, 2013 replaced the colonial-era Land Acquisition Act of 1894. Section 96 clearly states: “No income tax or stamp duty shall be levied on any award or agreement made under this Act.” Despite this clear language, tax authorities often contested the exemption on interest and solatium components. The Finance Bill, 2026 now removes any ambiguity. It provides a specific exemption provision for compulsory acquisition under the RFCTLARR Act.

Compensation vs. Solatium: Key Distinctions

Lawyers must distinguish between “compensation” and “solatium” when advising clients. Compensation refers to the market value of the land. Additionally, it includes the value of assets like crops and buildings. In contrast, solatium is an additional 100% payment on the market value. This payment recognizes the compulsory nature of the acquisition.

Previously, the tax department often treated interest on delayed payments as taxable income from other sources. However, the Supreme Court in Ghanshyam HUF v. CIT (2009) held differently. It ruled that interest under Section 28 forms part of the compensation value. This Budget 2026 land acquisition tax exemption extends to all these components. Furthermore, it overrides earlier limitations under Section 10(37) of the Income Tax Act. That section applied only to agricultural land.

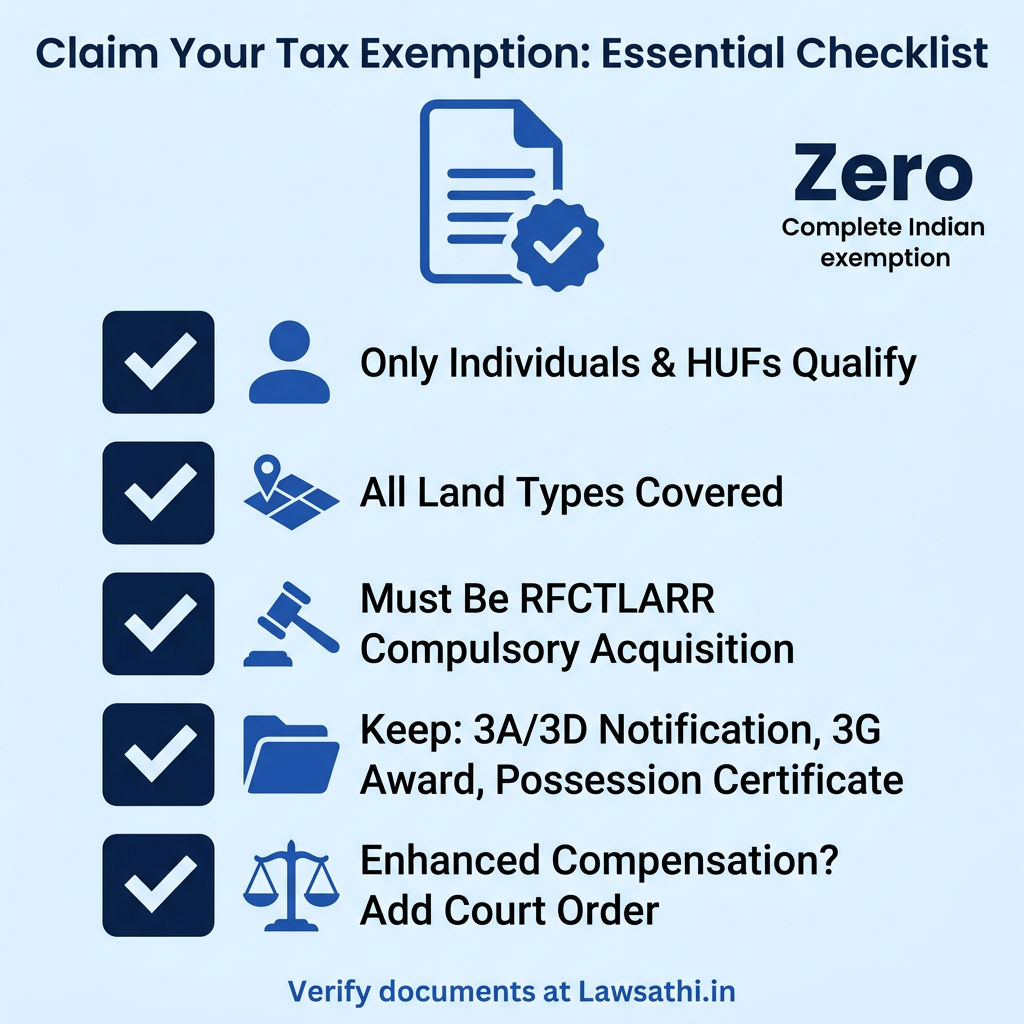

Who Qualifies? Eligibility Criteria for Tax Exemption

The new exemption is not available to all taxpayers. It specifically targets individuals and HUFs who receive compensation for land compulsorily acquired by the government. Therefore, corporate entities and partnership firms cannot claim this relief.

Defining the Eligible Recipient

The exemption covers “individuals and Hindu Undivided Families (HUFs).” Importantly, it does not use the term “farmer” as a strict legal definition. Instead, it focuses on the nature of the transaction—compulsory acquisition under the RFCTLARR Act. This distinction is crucial. For example, a non-farmer individual owning non-agricultural land that is acquired for a highway project also qualifies. The 81 FAQs on India’s Finance Bill (Budget) 2026 clarifies this point. Specifically, the nature of the recipient matters more than their occupation.

Scope of Land Coverage

The exemption covers any land acquired under the RFCTLARR Act, 2013. This includes: Agricultural land (both rural and urban) Non-agricultural land (residential, commercial, or industrial) * Any other immovable property

However, private acquisitions remain outside this scope. If a private company purchases land through negotiation, the transaction falls under standard capital gains provisions. Only government or statutory body acquisitions qualify.

Essential Documentation for Claims

Lawyers must ensure clients possess the correct documents to claim this exemption. Key documents include: 1. Section 3A/3D Notification: The government’s intent to acquire and declaration. 2. Section 3G Award: The compensation award passed by the Competent Authority. 3. Possession Certificate: Proof that the land has been handed over. 4. Bank Statements: Showing the credit of compensation amount.

As noted in the Income Tax Department’s tutorial on compulsory acquisition, proper documentation prevents future litigation. For enhanced compensation awarded by courts, lawyers must also attach the court order.

Types of Compensation Now Fully Exempt

Budget 2026 provides a comprehensive exemption that covers all components of the compensation package. This includes principal compensation, solatium, interest, and even enhanced compensation awarded by courts.

Breakdown of Exempt Amounts

The compensation structure under the RFCTLARR Act is multi-layered. The following components are now fully tax-exempt:

| Component | Description | Exemption Status | | :— | :— | :— | | Market Value | Circle rate or average sale price | Fully Exempt | | Multiplier Factor | 1x to 2x for rural areas | Fully Exempt | | Solatium | 100% of market value + assets | Fully Exempt | | Interest | 12% p.a. on market value | Fully Exempt | | Enhanced Comp. | Additional amount awarded by Court | Fully Exempt |

The Budget 2026 land acquisition tax exemption removes the need to segregate these amounts for tax purposes. Previously, disputes often arose regarding the taxability of interest. This was noted in analysis on Income Tax on Compulsory Acquisition.

Exclusion of Rehabilitation Benefits

Lawyers must note one critical exclusion. Rehabilitation and Resettlement (R&R) benefits under Section 46 of the RFCTLARR Act are not exempt. Section 96 specifically excludes Section 46 from the tax exemption. Therefore, benefits like annuities, employment for family members, or housing assistance may still have tax implications. However, the monetary compensation for the land itself remains fully tax-free.

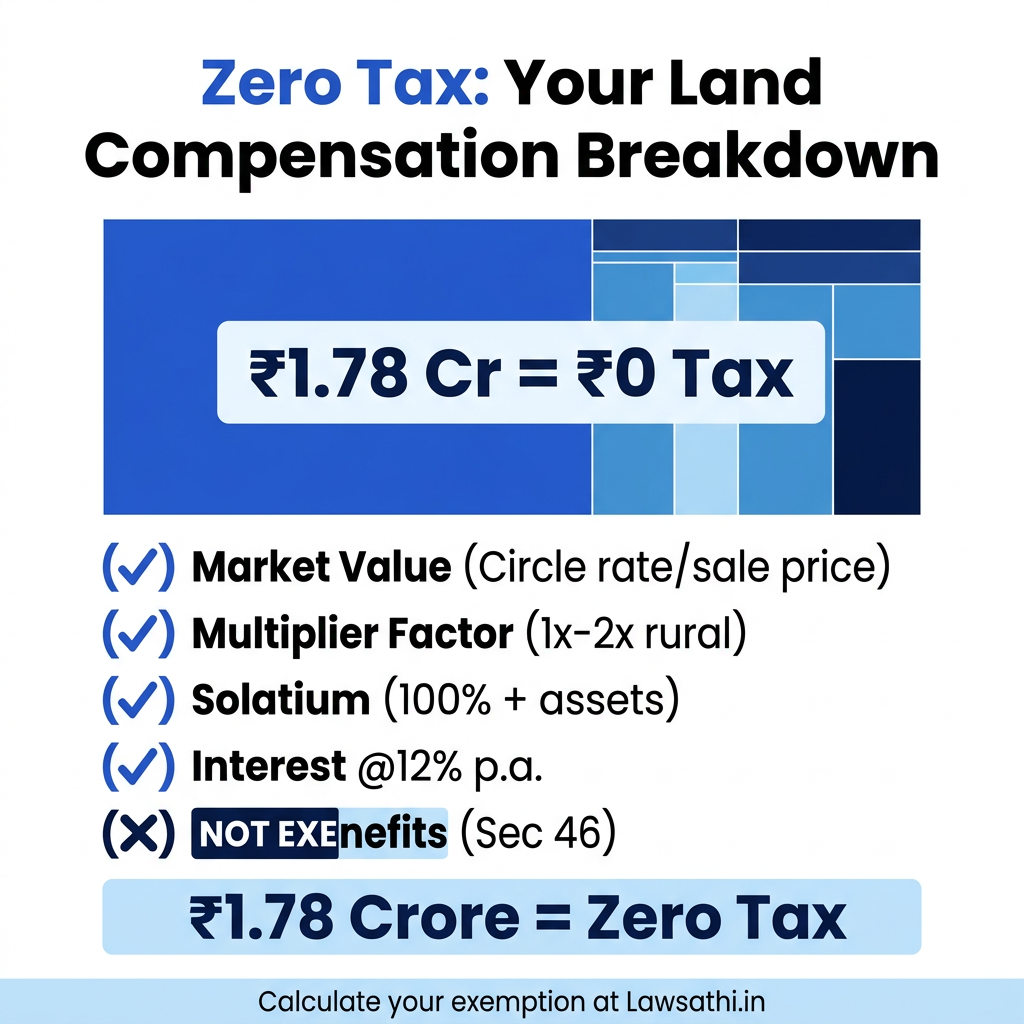

Real-World Calculation Example

Consider an individual whose land is acquired for a national highway project. Market Value Determined: ₹50,00,000 Multiplier Factor (Rural): 1.5 * Value of Assets (Trees, Well): ₹5,00,000

The calculation for exempt income would be: 1. Market Value + Multiplier: ₹50L × 1.5 = ₹75,00,000 2. Add Value of Assets: ₹5,00,000 3. Solatium (100%): ₹80,00,000 4. Interest (@12% for 2 years): ₹18,00,000

Total Exempt Compensation: ₹1,78,00,000. Consequently, the landowner pays zero tax on this entire amount.

Practical Implications for Law Firms and Legal Practice

This amendment creates immediate opportunities and challenges for law firms. Lawyers must pivot from tax litigation to advisory roles. The focus will shift from minimizing tax liability to maximizing compensation valuation.

Impact on Pending Litigation

Many ongoing disputes concern the taxability of solatium and interest. The Supreme Court’s recent dismissal of the NHAI review petition on February 23, 2026, clarified retrospective claims. According to Business Standard, pre-2018 cases cannot be reopened for interest claims. However, the government has settled the broader principle with the new exemption. Law firms should: Review all pending Income Tax Appellate Tribunal (ITAT) cases. Withdraw appeals where the tax department contested the exemption. * File for refunds in cases where tax was deposited under protest.

New Advisory Opportunities

Rural India will see a surge in demand for legal services related to land acquisition. Farmers now have a stronger incentive to contest low valuations. Since the entire amount is tax-free, every rupee of enhanced compensation directly benefits the client. As highlighted by Mondaq’s analysis of Budget 2026-27, this change reduces compliance burdens. However, it increases the need for valuation expertise. Law firms should: Offer services in Land Acquisition Reference cases. Assist clients in proving higher market values. * Advise on documentation to ensure seamless exemption claims.

Revision of Tax Planning Strategies

Earlier, lawyers advised clients to reinvest compensation in specified assets under Section 54 or 54F. This required detailed tracking of investment timelines. Under the new regime, such tax planning is largely unnecessary for compulsory acquisition. Clients can retain the full amount in fixed deposits or other instruments. Consequently, they need not worry about capital gains. Law firms must therefore update their advisory templates.

Documentation and Compliance Requirements

While the tax burden is removed, compliance remains essential. The Income Tax Department will require a clear declaration and proof of acquisition to allow the exemption.

Claiming the Exemption in ITR

Taxpayers must report this income correctly in their Income Tax Returns. While the amount is exempt, it should be disclosed under the “Exempt Income” schedule. The CBDT circular on land acquisition compensation provides guidance on reporting. Lawyers should advise clients to maintain a separate computation statement. This statement should show the breakdown of compensation.

Time Limits for Refund Claims

For clients who paid tax in previous years, claiming a refund is time-sensitive. The key options include: Section 237 (Refund): Must be filed within one year from the end of the assessment year. Section 154 (Rectification): Allowed within four years from the end of the financial year in which the order was passed. * Section 139(8A) (Updated Return): Can be filed within four years, but with additional tax.

As per Budget 2026 updates, the window for updated returns has been extended. Lawyers should therefore act swiftly to identify eligible cases.

Record-Keeping Best Practices

Law firms must implement robust record-keeping for land acquisition matters. Recommended practices include: 1. Retaining original award notifications for at least 8 years. 2. Storing bank statements showing compensation receipts. 3. Preserving court orders for enhanced compensation.

These records are vital not just for income tax compliance. Additionally, they prove useful for future land disputes.

Case Law Update: Impact on Pending Litigation

Several landmark judgments have shaped the jurisprudence on land acquisition compensation. Budget 2026 effectively endorses the pro-landowner view taken by courts in recent years.

Key Supreme Court Judgments Affected

In Tarsem Singh v. Union of India (2019), the Supreme Court held a significant view. It ruled that landowners under the National Highways Act are entitled to solatium and interest. This judgment created a significant financial liability for acquiring bodies. The Moneylife analysis on retrospective solatium discusses the implications of this ruling. Budget 2026’s exemption aligns with this judicial stance. As a result, landowners receive the full benefit.

Impact of the Chhattisgarh High Court Ruling

The Chhattisgarh High Court in Sanjay Kumar Baid v. ITO (September 2025) delivered a crucial verdict. It held that Section 96 of the RFCTLARR Act applies to acquisitions under the National Highways Act. The judgment stated that once compensation is determined under RFCTLARR provisions, the tax exemption follows. The High Court of Chhattisgarh judgment PDF_5.pdf) provides detailed reasoning. This decision, now supported by the Budget amendment, clarifies the position for all Fourth Schedule enactments.

Retrospective vs. Prospective Application

A key legal question remains: does this exemption apply retrospectively? The Finance Bill states it is effective from April 1, 2026. However, for compensation received before this date but litigated afterwards, the position requires clarification. Lawyers should await specific CBDT circulars. As noted by Devdiscourse, courts have generally favored a liberal interpretation for landowners. This suggests a strong case for applying the exemption to pending disputes.

Comparative Analysis: Previous Regime vs. Budget 2026

The shift from the old regime to the new framework is substantial. It simplifies the law and significantly increases the financial benefit for landowners.

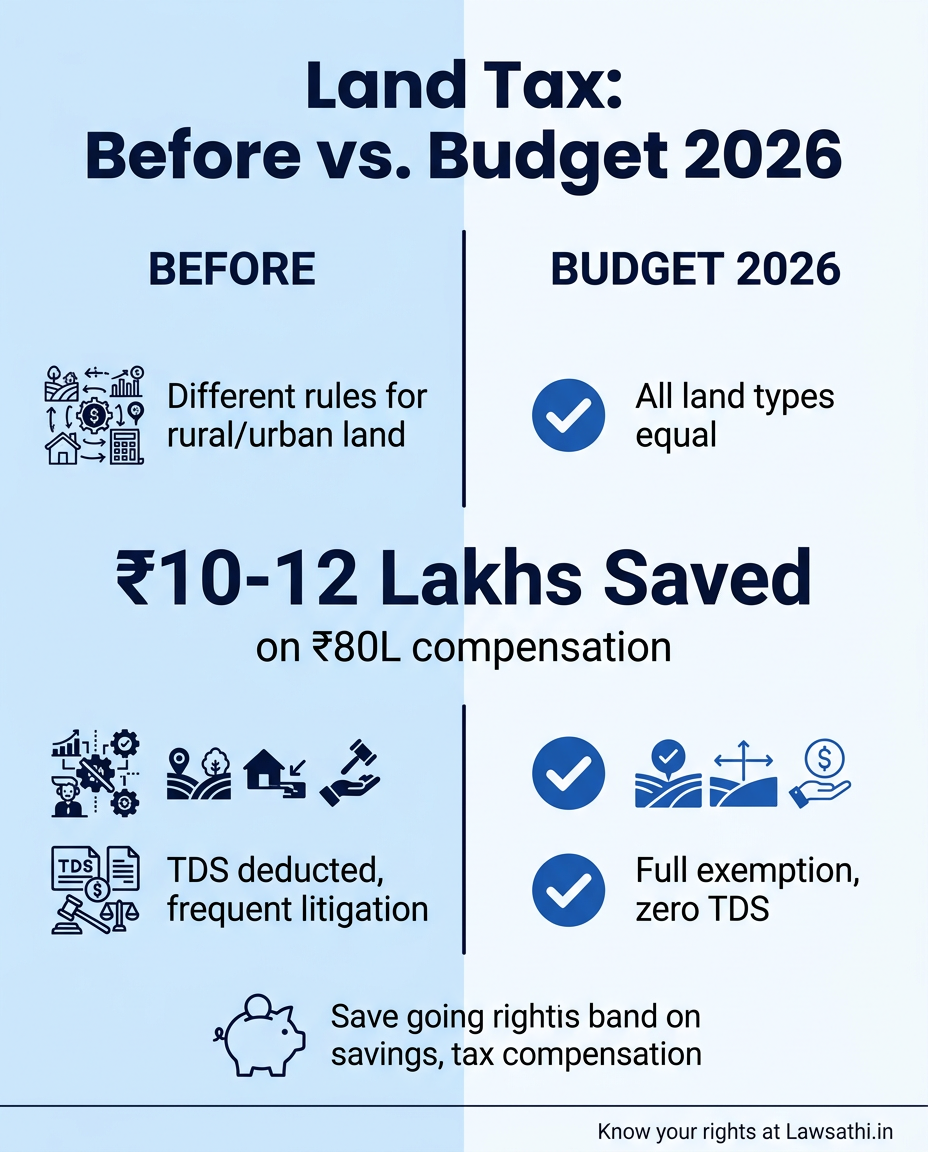

Taxation Before Budget 2026

Under the previous regime, tax liability depended on the type of land. Rural Agricultural Land: Not a capital asset; no capital gains tax. Interest was often contested. Urban Agricultural Land: Exempt under Section 10(37) if used for agriculture for 2 years. * Non-Agricultural Land: Fully taxable as capital gains. TDS was deducted under Section 194LA.

Litigation frequently arose over the distinction between Section 28 interest (compensation) and Section 34 interest (delay). As seen in cases like No Section 263 Revision When Two Views Possible, even the tax department was unclear on the position.

The New Regime: A Simplified Framework

Budget 2026 eliminates these distinctions for compulsory acquisition. All Land Types: Treated equally. Interest & Solatium: Fully exempt. * TDS: Should no longer be deducted for RFCTLARR acquisitions.

This Budget 2026 land acquisition tax exemption reduces the compliance burden. Furthermore, it lowers litigation costs significantly.

Financial Benefit Calculation: A Comparison

Let’s compare the tax liability for a non-agricultural land acquisition.

Scenario: Urban residential plot acquired for ₹80 lakhs (including solatium).

| Parameter | Previous Regime | Budget 2026 Regime | | :— | :— | :— | | Compensation | ₹80,00,000 | ₹80,00,000 | | Taxable Income | Capital Gains + Interest | Zero | | Approximate Tax (LTCG) | ₹10-12 lakhs | ₹0 | | Net Benefit to Landowner | Reduced by Tax | Full Amount |

The savings are substantial, often running into lakhs for small landowners. States like Maharashtra, Gujarat, and Uttar Pradesh will see the maximum impact. These states have high infrastructure activity, as noted in PIB reports on land acquisition.

Conclusion: What Lawyers Need to Do Now

Budget 2026 marks a new era for land acquisition law in India. The complete tax exemption empowers farmers and simplifies legal practice. However, lawyers must take proactive steps to leverage this change for their clients.

Immediate Action Plan for Law Firms

Lawyers should start by reviewing their client databases. Identify all clients with ongoing land acquisition matters. Additionally, find those who paid tax in the last four years. Prepare a standardized advisory note explaining the Budget 2026 land acquisition tax exemption. Furthermore, monitor CBDT notifications for clarifications on documentation and time limits.

This amendment reduces the need for complex tax planning. However, it increases the importance of proper valuation. Law firms should collaborate with valuation experts to help clients claim fair compensation. Since the entire amount is now tax-free, maximizing the valuation has become even more critical.

Stay ahead of revenue law updates with LawSathi’s AI-powered legal research and practice management tools. Get real-time alerts on tax law amendments, automated case tracking for land acquisition matters, and client communication templates. Start your 14-day free trial today.