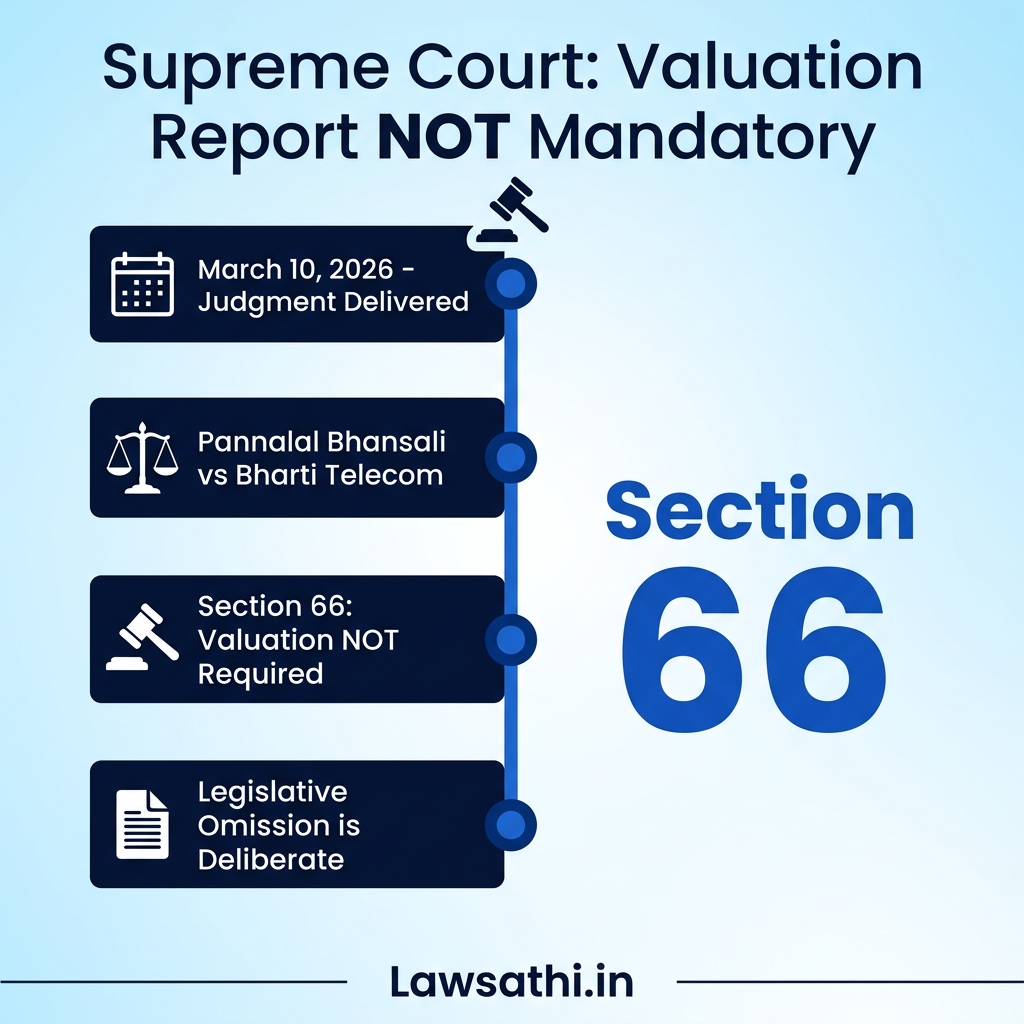

The Supreme Court delivered a landmark judgment on March 10, 2026. Specifically, the Court holds valuation report not mandatory for reduction of share capital under Companies Act Section 66. This ruling in Pannalal Bhansali Versus Bharti Telecom Limited & Ors. brings significant clarity. In fact, it benefits corporate lawyers and companies undertaking capital reduction exercises.

Furthermore, the judgment clarifies an important point. While obtaining a valuation report may be prudent, it is not a statutory requirement under Section 66 of the Companies Act, 2013.

Introduction: Understanding the Landmark Ruling

The Supreme Court’s recent decision addresses a crucial question. For years, this question has troubled corporate practitioners. Does Section 66 mandate a valuation report when a company decides to reduce its share capital? Finally, the apex court answered this question definitively.

A bench comprising Justices Sanjay Kumar and K. Vinod Chandran delivered this important judgment. Justice K. Vinod Chandran authored the detailed reasoning. Consequently, his analysis clarifies the legislative intent behind Section 66.

The Core Legal Question Before the Court

The central issue concerned a specific requirement. Namely, must companies obtain and circulate a valuation report before reducing share capital? This question arose from a challenge by minority shareholders. They alleged procedural deficiencies in Bharti Telecom’s capital reduction exercise.

The petitioners claimed the company failed to disclose the valuation report to shareholders. They argued this non-disclosure vitiated the entire process. However, the Supreme Court disagreed with this interpretation of the law.

Case Background: Bharti Telecom’s Capital Reduction

Bharti Telecom Limited decided to reduce shares held by certain public shareholders. This decision formed part of a capital reduction exercise. Accordingly, the company planned to compensate affected shareholders monetarily for their shares.

The company obtained an external valuation. As a result, share value was determined at ₹163.25 per share. This valuation applied a Discount for Lack of Marketability (DLOM). Specifically, the discount applied because the shares were unlisted and illiquid.

The Valuation Dispute Arises

A separate fairness report from another financial entity supported this valuation. However, the National Company Law Tribunal intervened in the matter. The NCLT increased the payout to ₹196.80 per share while approving the capital reduction.

Despite overwhelming shareholder approval, certain minority shareholders challenged the process. They alleged the valuation was fundamentally unfair. Additionally, they claimed the company should have disclosed the valuation report with the meeting notice.

Supreme Court’s Key Observations on Section 66

The Supreme Court holds valuation report not mandatory for reduction of share capital under Companies Act Section 66. To reach this conclusion, the Court examined the legislative scheme of the Companies Act, 2013.

The bench observed that Section 66 contains specific requirements. Notably, it omits any valuation report mandate. According to the Court’s analysis, this omission is deliberate and meaningful.

Distinguishing Section 66 from Other Provisions

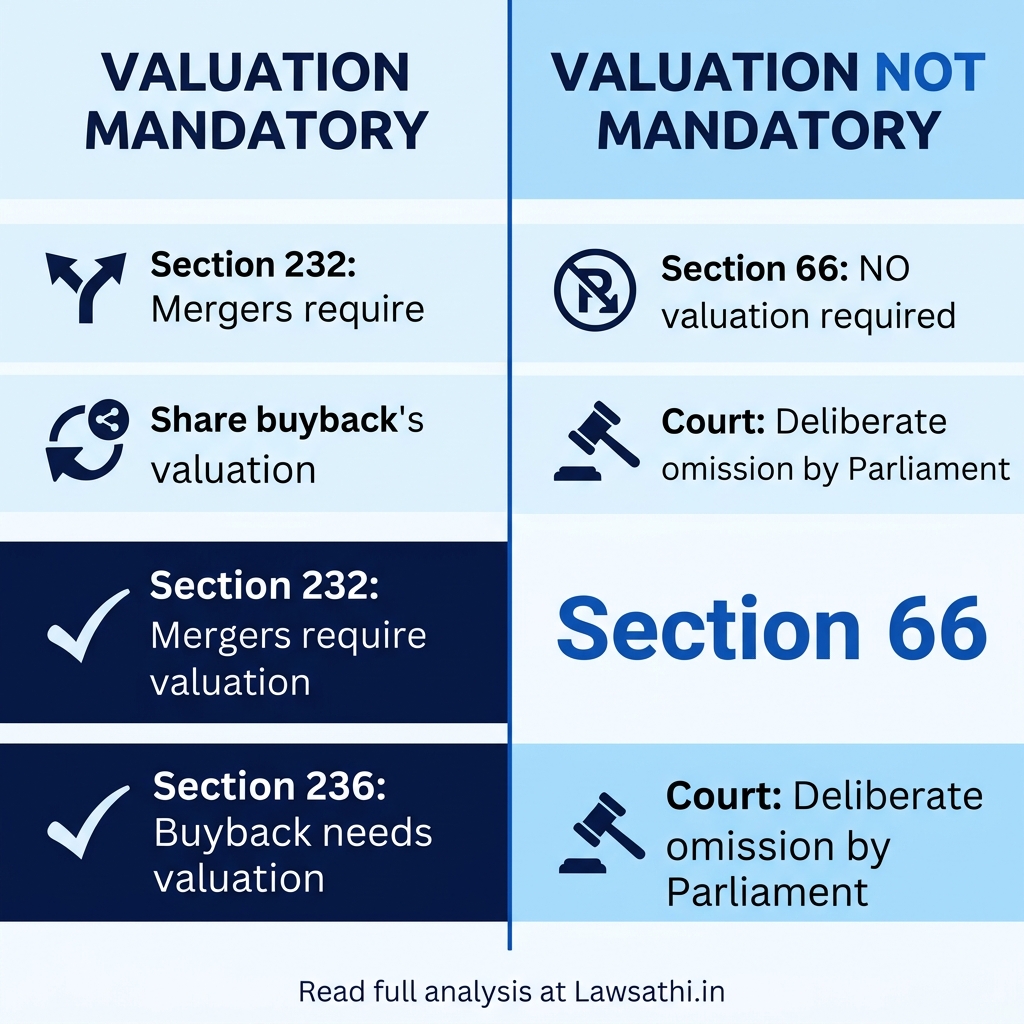

The Court compared Section 66 with other provisions of the Companies Act. Specifically, it examined provisions where valuation IS mandatory. This comparison proved illuminating for understanding legislative intent.

Notably, the Court pointed out an important distinction. Section 236(2) requires valuation in the context of buyback or purchase of minority shares. However, this requirement is “conspicuously absent” in Section 66. This absence persists even though capital reduction also results in exit of certain shareholders.

The Court’s Exact Words on Non-Disclosure

The Supreme Court stated its position clearly. “We do not think that the notice in the present case is vitiated by non-disclosure or mis-disclosure merely for reason of the valuation and fairness report not being placed before the shareholders.”

Furthermore, the Court emphasized another key point. “Reduction of share capital can be achieved by a special resolution and confirmation by the Tribunal, without a report of valuation from an approved/registered valuer.”

Understanding Section 66 Requirements

Section 66 of the Companies Act, 2013 prescribes a specific procedure for capital reduction. The Supreme Court holds valuation report not mandatory for reduction of share capital under Companies Act Section 66. This conclusion is based on the statutory scheme.

In particular, the provision requires companies to follow several mandatory steps. These steps ensure adequate protection for shareholders and creditors during the capital reduction process.

Mandatory Requirements Under Section 66

The following requirements are statutorily mandated under Section 66:

1. Special Resolution by shareholders approving the reduction 2. Confirmation by Tribunal (NCLT) after due process 3. Notice to Central Government, Registrar, SEBI (for listed companies), and creditors 4. Consideration of representations received within 3 months 5. Tribunal satisfaction that creditor claims are discharged, determined, or secured 6. Accounting treatment conforming to standards under Section 133 7. Auditor’s certificate filed with the Tribunal 8. Publication of order as directed by Tribunal 9. Filing with Registrar within 30 days of order

Notably absent from this list is any requirement for valuation report from a registered valuer.

Standard for Challenging Expert Valuation

The Supreme Court also addressed another important issue. Specifically, when can courts and tribunals interfere with expert valuations? This guidance is crucial for lawyers handling capital reduction matters.

In general, the Court established that expert valuation should ordinarily not be interfered with. However, interference is justified in specific circumstances.

When Can Valuation Be Challenged?

Valuations can be challenged only if demonstrated to be:

– Manifestly erroneous in methodology or application – Biased in favor of certain parties – Illegal in terms of applicable legal principles

In the Bharti Telecom case, none of these grounds were established by the petitioners. Therefore, the Court upheld the valuation methodology employed by the company.

Practical Implications for Corporate Lawyers

This judgment has significant practical implications for Indian legal professionals advising companies. Most importantly, the Supreme Court holds valuation report not mandatory for reduction of share capital under Companies Act Section 66. Consequently, this reduces regulatory burden.

However, lawyers should understand the nuanced position the Court has taken. The ruling does not discourage obtaining valuation reports altogether.

Advisory Points for Companies

First, companies now have clear flexibility to proceed with share capital reduction. They need not obtain or circulate valuation reports as a mandatory requirement.

Second, obtaining a valuation report remains advisable as a matter of prudence. Such reports provide objective evidence of fair treatment of shareholders.

Third, the two-step process remains unchanged. Companies must pass a special resolution and obtain Tribunal confirmation.

Implications for Minority Shareholders

Minority shareholders cannot challenge capital reduction on certain grounds. Specifically, they cannot challenge solely based on non-disclosure of valuation reports. This provides certainty to companies undertaking such exercises.

However, shareholders retain the right to challenge valuations on substantive grounds. They must demonstrate the valuation is manifestly erroneous, biased, or illegal.

Role of Tribunals Under Section 66

The NCLT retains significant authority to protect shareholder interests. For example, in this case, the Tribunal increased compensation from ₹163.25 to ₹196.80 per share. Remarkably, it did so without requiring a fresh valuation.

This demonstrates that Tribunal oversight provides meaningful protection. The process does not become unfair simply because valuation reports are not mandatory.

Legislative Intent Behind Section 66

The Supreme Court’s analysis reveals clear legislative intent behind Section 66. Notably, Parliament chose not to include valuation report requirement. This choice was made despite including it in similar provisions.

In other words, this legislative choice reflects different policy considerations for capital reduction. The Court respected this deliberate legislative decision in its interpretation.

Comparing with the 1956 Act

Under the Companies Act, 1956, capital reduction also did not mandate valuation reports. The 2013 Act maintained this position. Significantly, it maintained this even while adding valuation requirements elsewhere.

The legislative history supports the Court’s interpretation. Parliament could have easily included such a requirement. Instead, it deliberately chose not to.

Best Practices for Capital Reduction

The Supreme Court holds valuation report not mandatory for reduction of share capital under Companies Act Section 66. Nevertheless, companies should follow best practices.

For instance, prudence suggests obtaining independent valuation reports in most cases. This protects against potential challenges and demonstrates fair dealing.

Recommended Approach for Companies

Companies should consider the following approach:

1. Obtain independent valuation even though not mandatory 2. Disclose key valuation findings to shareholders for transparency 3. Ensure fair treatment of all shareholder classes 4. Document decision-making process thoroughly 5. Prepare for Tribunal scrutiny of the entire process

Following these practices helps ensure smooth approval and minimize litigation risk.

The Outcome of the Bharti Telecom Case

The Supreme Court dismissed all appeals in this matter. Therefore, the capital reduction approved by NCLT and NCLAT was upheld as valid.

This outcome confirms that companies following proper procedure under Section 66 need not fear reversal. The absence of valuation report does not invalidate the process.

Key Takeaways from the Judgment

The judgment in Pannalal Bhansali Versus Bharti Telecom Limited (2026 LiveLaw (SC) 222) establishes several important principles:

1. Valuation report is NOT mandatory under Section 66 2. Legislative intent is clear from absence of such requirement 3. Special resolution plus Tribunal confirmation remains the required process 4. Valuation reports may be obtained as matter of prudence 5. Tribunals can protect shareholder interests through compensation adjustments 6. Expert valuations should not be interfered with absent proven deficiencies

Conclusion

The Supreme Court holds valuation report not mandatory for reduction of share capital under Companies Act Section 66. Undoubtedly, this judgment provides much-needed clarity. Additionally, this ruling reduces regulatory burden while maintaining adequate protections through Tribunal oversight.

Corporate lawyers should advise clients accordingly. While valuation reports are not legally required, obtaining them remains prudent practice. The two-step process of special resolution and Tribunal confirmation continues to govern capital reduction exercises.

In summary, this judgment represents a balanced approach. It respects legislative intent while preserving mechanisms for shareholder protection. Indian businesses can now proceed with capital reduction exercises with greater certainty about procedural requirements.

Streamline Your Corporate Law Practice with LawSathi

Managing corporate law matters requires meticulous documentation and deadline tracking. LawSathi helps you organize case files, track Tribunal deadlines, and manage client communications efficiently. Our AI-powered platform is designed specifically for Indian legal professionals.

Try LawSathi free for 15 days and experience how technology can transform your practice.