Mastering the ITAT appeal filing procedure is essential for every tax litigator practicing in India. The Income Tax Appellate Tribunal serves as the first independent quasi-judicial forum. Furthermore, it examines the correctness of tax officers’ decisions. Additionally, ITAT holds the unique distinction of being the last fact-finding authority in the tax litigation hierarchy. This comprehensive guide covers everything from drafting valid grounds of appeal to navigating limitation periods. Specifically, it addresses requirements under Section 253 of the Income Tax Act, 1961.

Introduction: The Role of ITAT in Indian Tax Litigation

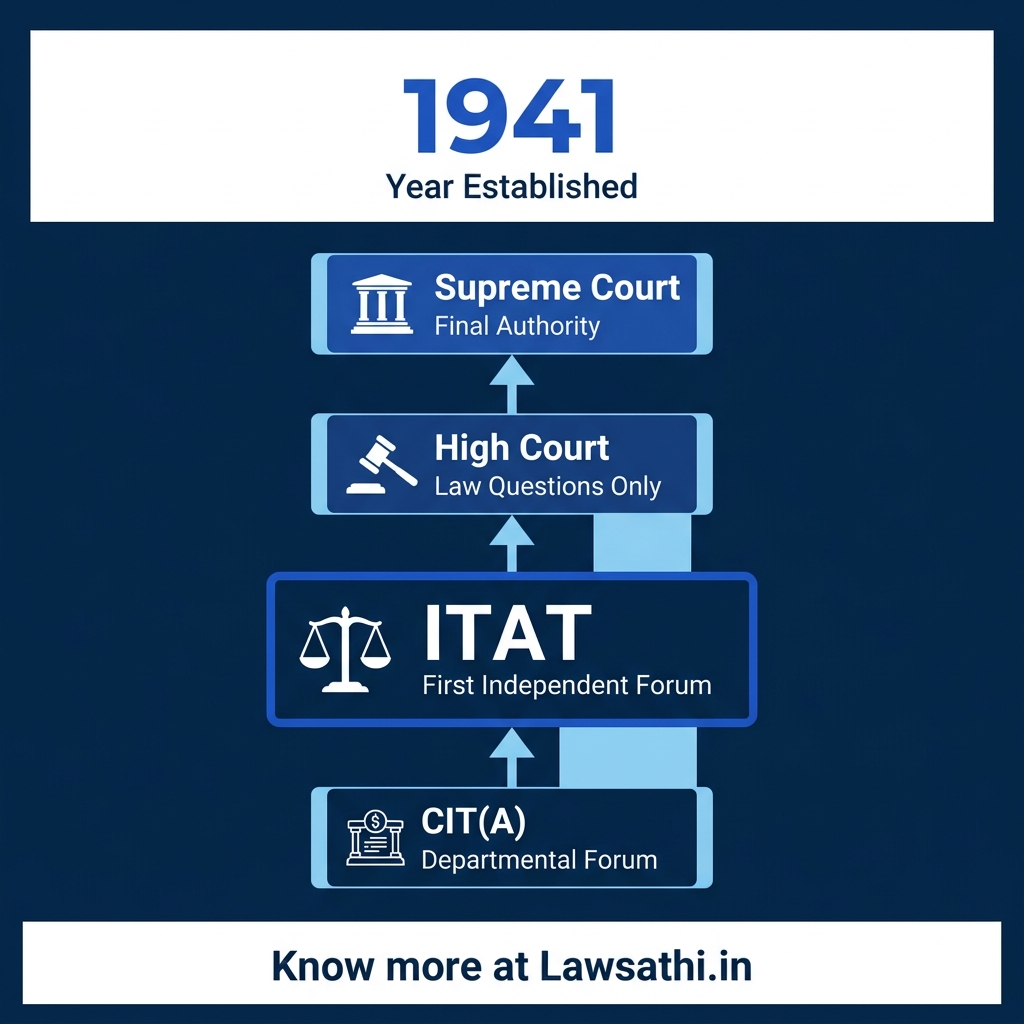

The Position of ITAT in the Appeal Hierarchy

The Income Tax Appellate Tribunal was established in January 1941. Therefore, it ranks among India’s oldest tribunals. Initially, it operated with just 6 Members across 3 Benches in Delhi, Kolkata, and Mumbai. However, ITAT has expanded significantly today. It now has Benches across major cities nationwide.

The Tribunal occupies a critical position in the tax appeal hierarchy. An assessee dissatisfied with an Assessment Officer’s order first approaches the Commissioner of Income Tax (Appeals). However, CIT(A) remains part of the departmental structure. Therefore, ITAT becomes the first truly independent forum for taxpayers seeking justice.

Why ITAT Matters for Tax Litigators

According to SCC Online Blog, “The Tribunal is the first intrinsically independent forum which examines the correctness of the views and positions taken by the tax officers.” This independence makes ITAT the most crucial forum for factual disputes.

Moreover, ITAT’s factual determinations bind even the High Court and Supreme Court unless proven perverse. Consequently, tax litigators must present factual arguments comprehensively before ITAT. Appeals to High Court under Section 260A lie only on substantial questions of law.

This guide provides a complete roadmap covering grounds of appeal, limitation periods, Form 36 requirements, and procedural compliance for 2026.

Determining Valid Grounds of Appeal: Questions of Law vs. Fact

Understanding ITAT’s Jurisdiction

Unlike High Courts, ITAT can entertain both questions of law and questions of fact. This broad jurisdiction makes the ITAT appeal filing procedure distinct from subsequent appeals. Furthermore, the Tribunal serves as the last fact-finding authority in tax litigation.

However, this freedom comes with responsibility. Grounds must be drafted precisely to survive scrutiny. The ITAT Office Manual explicitly specifies that grounds “shall set forth, concisely and under distinct heads, the grounds of appeal without any argument or narrative.”

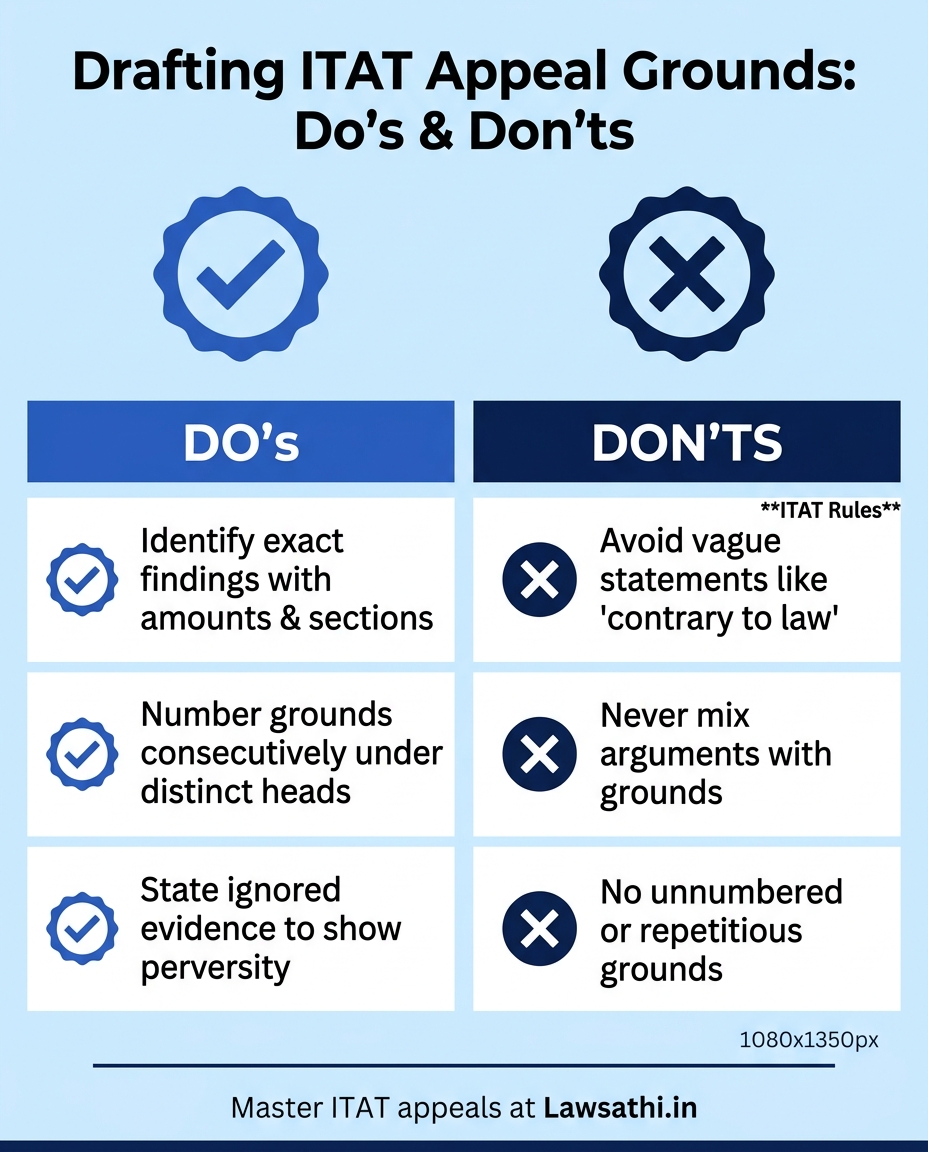

Drafting Effective Grounds of Appeal

Specific vs. Vague Grounds

Vague allegations without particulars lead to immediate dismissal. For example, stating “the order is contrary to law” without specifying how provides no basis for adjudication. Instead, grounds should identify the exact finding challenged.

Consider this well-drafted ground: “The CIT(A) erred in confirming the addition of Rs. 15 lakhs under Section 68 without considering the documentary evidence of share application money received from identified parties.”

Challenging Findings of Fact

Since ITAT is the last fact-finding authority, factual determinations require special attention. Merely disagreeing with findings won’t suffice. Therefore, you must demonstrate perversity or lack of consideration of material evidence.

For instance, if the Assessing Officer ignored bank statements proving genuine transactions, this constitutes perversity. The ground should specifically state what evidence was ignored. Additionally, it should explain the evidence’s relevance.

Common Mistakes That Lead to Dismissal

Tax litigators frequently commit avoidable errors when drafting grounds. First, repetitious grounds waste precious judicial time. They merely rehash arguments presented before CIT(A). Second, failure to specify exact findings creates confusion.

Third, not explaining how a factual finding is perverse weakens the appeal significantly. Fourth, mixing arguments with grounds violates the ITAT Rules explicitly. Finally, unnumbered grounds create procedural defects that may delay listing.

The Critical Timeline: Limitation Period for Filing ITAT Appeals

Statutory Framework Under Section 253

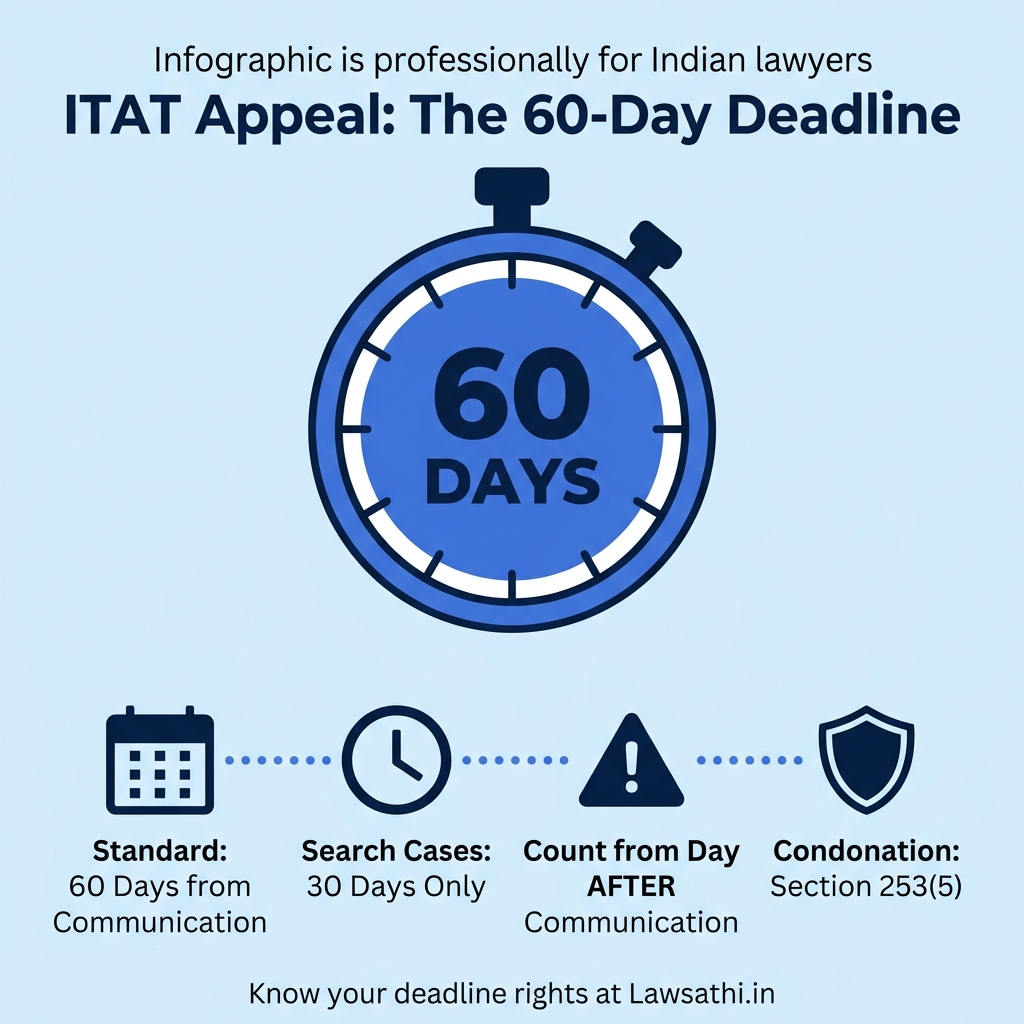

The Income Tax Act, 1961 prescribes strict limitation periods for ITAT appeals. Section 253(3) mandates that appeals must be filed within 60 days. This period starts from the date of communication of the order.

This 60-day period applies to appeals against CIT(A) orders under Section 250. Similarly, appeals against Commissioner’s revision orders under Section 263 follow the same timeline. However, search cases under Section 158-BC have a shorter 30-day limit.

Calculating the Limitation Period Correctly

Understanding the calculation methodology prevents costly mistakes. The limitation period begins from the date of communication. Importantly, it does not start from the date of the order itself. This distinction matters significantly in practice.

For example, consider this scenario. CIT(A) passes an order on January 15, 2026. However, the order is communicated on February 1, 2026. In this case, the 60-day period starts from February 2, 2026. The date of communication gets excluded from calculation.

Different Timelines for Different Orders

| Type of Order | Limitation Period | Governing Provision | |————–|——————-|———————| | CIT(A) order under Section 250 | 60 days | Section 253(3) | | Commissioner’s revision under Section 263 | 60 days | Section 253(3) | | Search cases under Section 158-BC | 30 days | Proviso to Section 253(3) | | Cross-objections | 30 days | Section 253(4) |

Therefore, tax litigators must identify the correct timeline based on the order type. Missing the deadline without sufficient cause can be fatal to the appeal.

Condonation of Delay: Salvaging Time-Barred Appeals

Legal Provision for Late Filing

Section 253(5) empowers ITAT to admit appeals filed after the limitation period. However, the Tribunal must be satisfied that “sufficient cause” existed for the delay. This provision mirrors Section 5 of the Limitation Act.

The standard for condonation isn’t merely procedural compliance. Rather, courts have interpreted “sufficient cause” liberally. They do so to advance substantial justice.

The Landmark N. Balakrishnan Standard

The Supreme Court’s decision in N. Balakrishnan vs. M. Krishnamurthy (1998) 7 SCC 123 remains the governing precedent. The Court established several crucial principles.

First, the words “sufficient cause” should receive liberal construction. Second, there’s no presumption that delay is always deliberate. Third, courts must show consideration if the explanation doesn’t smack of mala fides.

Importantly, the length of delay alone isn’t determinative. The acceptability of the explanation matters most. As the Court noted, “In every case of delay there can be some lapse on the part of the litigant concerned. That alone is not enough to turn down his plea.”

Practical Application and Recent Cases

Recent ITAT decisions illustrate how these principles apply in practice. In the Visakhapatnam ITAT case reported by LiveLaw, condonation was rejected. Specifically, the assessee failed to substantiate reasons for delay.

Similarly, in Prerti Madhok v. ITO, ITAT dismissed a 581-day delay. The Tribunal noted that the appellant had engaged multiple CAs. This indicated awareness of legal processes.

However, in Bando India Pvt. Ltd. (Delhi ITAT, February 2025), a 1014-day delay was condoned. The assessee had filed a rectification application. Furthermore, it was exhausting alternate remedies. This demonstrates that genuine reasons can overcome even significant delays.

Documents Required for Condonation Applications

Successful condonation applications require supporting evidence. The ITAT E-Filing Portal mandates an affidavit explaining reasons for delay. Additionally, documentary evidence supporting the cause strengthens the application.

A timeline of events helps establish bona fides. Specifically, it should show when knowledge was acquired. Mere assertions without evidence rarely succeed before ITAT.

Form Requirements: Mastering Form No. 36 and Accompanying Documents

Essential Components of Form 36

Form No. 36 serves as the memorandum of appeal before ITAT. The official Form 36A format requires specific mandatory fields.

These include the appellant’s name, PAN, and complete address with PIN code. Additionally, phone and email details must be provided. Furthermore, respondent details, appeal number, and assessment year must be specified. The section under which the order was passed is also required.

The form also requires the total income declared. Moreover, amounts disputed with breakup must be detailed. Each ground must specify its tax effect separately.

Mandatory Documents Checklist

The ITAT E-Filing Portal prescribes mandatory and optional documents. For appeals against orders under Section 250, mandatory documents include:

1. Assessment Order under Section 153A/153C 2. Limitation Certificate and Letter of Authority 3. Tribunal Fee Challan 4. Grounds of Appeal before CIT(A) 5. Order of CIT(A) under Section 250 6. Grounds of Appeal before ITAT 7. Memorandum of Appeal (Form 36)

Optional documents include vakalatnama and covering letter. Additionally, statement of facts and condonation petitions may be attached if applicable.

Paper Book Requirements

The memorandum must be submitted in triplicate according to Form 36A requirements. The document should be written in English or Hindi in notified states. Furthermore, grounds must be numbered consecutively and presented under distinct heads.

Crucially, grounds should contain no argument or narrative. This procedural requirement appears in the ITAT Office Manual explicitly.

E-Filing Procedure for 2026

The ITAT E-Filing Portal has streamlined the filing process significantly. Assessees can login using OTP or Pre-Validated Code (PVC). Pre-validation of email and mobile generates PVCs valid for one month.

The Appeal Dashboard allows viewing e-filing details. Additionally, users can rectify defects and file additional documents. Tax litigators should regularly monitor this dashboard for defect notices.

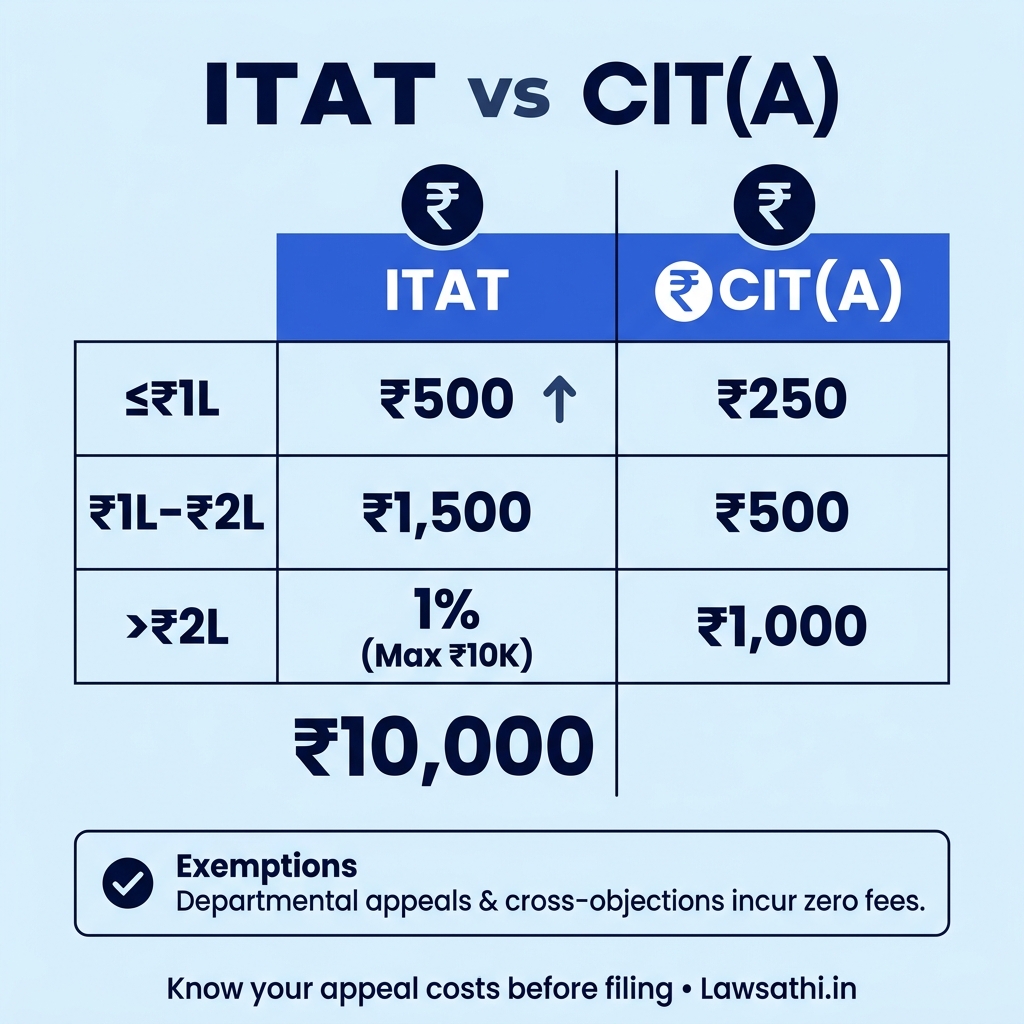

Fee Structure and Payment Procedure

Statutory Fee Slabs Under Section 253(6)

The Income Tax Act prescribes slab-wise appeal fees based on assessed income. For assessed income of Rs. 1,00,000 or less, the fee is Rs. 500.

For income exceeding Rs. 1,00,000 but not exceeding Rs. 2,00,000, the fee increases to Rs. 1,500. Where assessed income exceeds Rs. 2,00,000, the fee is 1% of assessed income. However, this is subject to a maximum of Rs. 10,000.

For other matters not covered above, the fee is Rs. 500. Importantly, departmental appeals under Section 253(2) are exempt from fees. Similarly, cross-objections under Section 253(4) require no fee payment.

Comparison With CIT(A) Fees

Understanding the fee differential helps in client counseling. Section 249 prescribes lower fees for CIT(A) appeals. For income up to Rs. 1,00,000, the CIT(A) fee is only Rs. 250.

For income between Rs. 1,00,000 and Rs. 2,00,000, CIT(A) fee is Rs. 500. For income exceeding Rs. 2,00,000, CIT(A) fee is Rs. 1,000. Consequently, this progression is significantly lower than ITAT fees.

Payment Mode and Documentation

Fees must be paid online through challan payment. Form 36 requires BSR code and date of payment. Additionally, challan serial number and amount must be specified. Defective fee payment triggers defect notices from the Tribunal.

Consequently, tax litigators should verify challan details before filing. The fee payment is mandatory for numbering of the appeal.

Conclusion: Best Practices for Tax Litigators

Pre-Filing Checklist

The ITAT appeal filing procedure demands meticulous attention to detail. Before filing, verify the limitation calculation using the date of communication. If delayed, prepare a comprehensive condonation application with supporting affidavit.

Review grounds for specificity. Furthermore, ensure they’re numbered consecutively under distinct heads. Each ground should identify the exact finding challenged. Additionally, specify its tax effect. Verify all mandatory documents are attached.

Calculate fees correctly based on assessed income. Moreover, preserve challan details carefully. Pre-validate credentials on the ITAT portal before attempting to file.

Technology for Deadline Management

Managing multiple appeal deadlines manually invites errors. Calendar alerts for limitation dates provide basic protection. However, dedicated case management software offers superior tracking capabilities.

Regular monitoring of the ITAT Appeal Dashboard helps catch defect notices early. The e-filing system’s Pre-Validated Code feature speeds up repeat filings.

Key Takeaways

ITAT remains the last fact-finding authority in tax litigation. Therefore, present factual arguments comprehensively. Additionally, challenge perversity specifically. The 60-day limitation period is strict. However, condonation is available for genuine causes.

“Sufficient cause” requires evidence, not mere assertions. Furthermore, procedural compliance including Form 36 requirements is non-negotiable. Mastering these elements distinguishes successful tax litigators from the rest.

Missed an ITAT deadline? Never let limitation periods slip through the cracks again. Automate your tax litigation workflow, manage case documents, and track critical appeal deadlines with LawSathi. Request a demo today.